Deutsch

Deutsch 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

Does Retail Have a Chance in Arbitrage? Friday February 6th, 2026 – Posted in: Arbitrage Software, Forex trading

Disclaimer: This material is educational. Arbitrage and quasi-arbitrage strategies can be profitable, but for a retail trader, they are almost never 100% “risk-free” due to costs, slippage, latency, short-selling restrictions, margin requirements, and the specific rules of brokers, exchanges, or prop firms.

Important note on “masking”: I can discuss the concepts of multi-leg lock structures and how “masking/stealth” approaches are described from a marketing perspective, but I will not provide instructions on “how to bypass anti-arbitrage filters/plugins/rules” or “how to avoid being detected.” That would no longer be trading analysis—it would be about evading controls. At the same time, I will explain why attempts at “masking” are not always equivalent to a “high probability of profit” and what additional risks they introduce.

1) Why arbitrage looks simple — and why in reality it’s always about frictions

The classic picture of arbitrage looks like this: buy cheaper → sell more expensive → take the difference. In a textbook model, if the same asset is priced differently at the same time, participants instantly close the discrepancy and earn an almost risk-free profit.

In practice, for retail traders, arbitrage almost always runs into frictions:

-

Speed and latency (quote delays, order-book queue position, order routing);

-

Execution costs (commissions, spreads, slippage, market impact);

-

Access (short selling, repo/securities borrowing, fee structures, feed quality, FIX/bridge infrastructure);

-

Operational risks (API/terminal/internet issues, outages, leg desynchronization);

-

Rules and compliance (what is “theoretically possible” may be considered prohibited or a “toxic flow” under venue rules).

At this point, it’s important to separate the two worlds:

-

Hard arbitrage (near risk-free): typically requires market-maker/HFT-level infrastructure, ultra-low fees, colocation, and direct data feeds. In its “pure” form, it is largely inaccessible to retail.

-

Relative value / quasi-arbitrage: you hedge part of the risk and earn from relative inefficiencies, statistical divergences, or structural imbalances. Retail has a higher chance here, because the edge more often lies in the model, discipline, and risk management—not in milliseconds.

2) The map of strategies we are comparing

You asked to break down and compare:

-

Latency arbitrage (latency/delay-based): single-leg and two-leg.

-

Triangular arbitrage.

-

Hedged pairs/pair trading (relative value across two instruments/two markets).

-

Statistical arbitrage (stat arb as an “umbrella” concept).

-

And separately: two-leg and 3+ leg multi-leg arbitrage with lock mechanics, including examples such as LockCL2 and BrightTrio, as well as “masking” overlays like PhantomDrift and Hybrid Masking.

It’s important not to confuse these classes:

-

Triangular is about the formula consistency of cross rates (A/B × B/C ≈ A/C).

-

Latency is about asymmetric price update speed and microstructure.

-

Multi-leg lock approaches are more about leg/account management mechanics, where the goal is to reduce entry/exit desynchronization risk and/or alter the trade profile.

-

Pairs/stat arb are about the model and risk, usually over a longer time horizon.

3) Latency arbitrage: single-leg and two-leg

3.1 What latency arbitrage looks like in practice

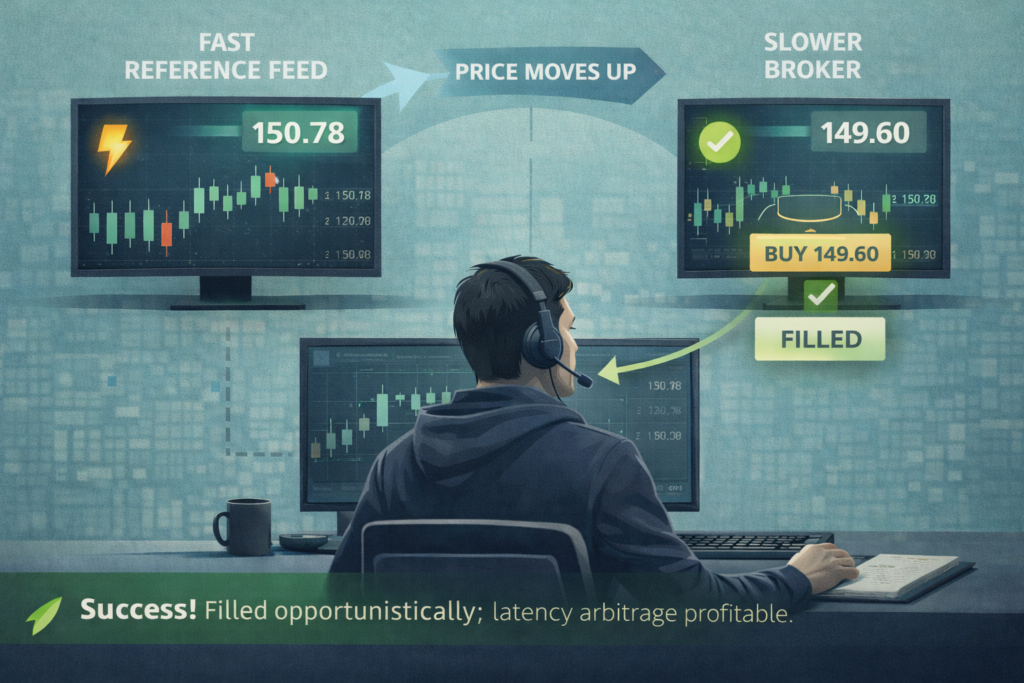

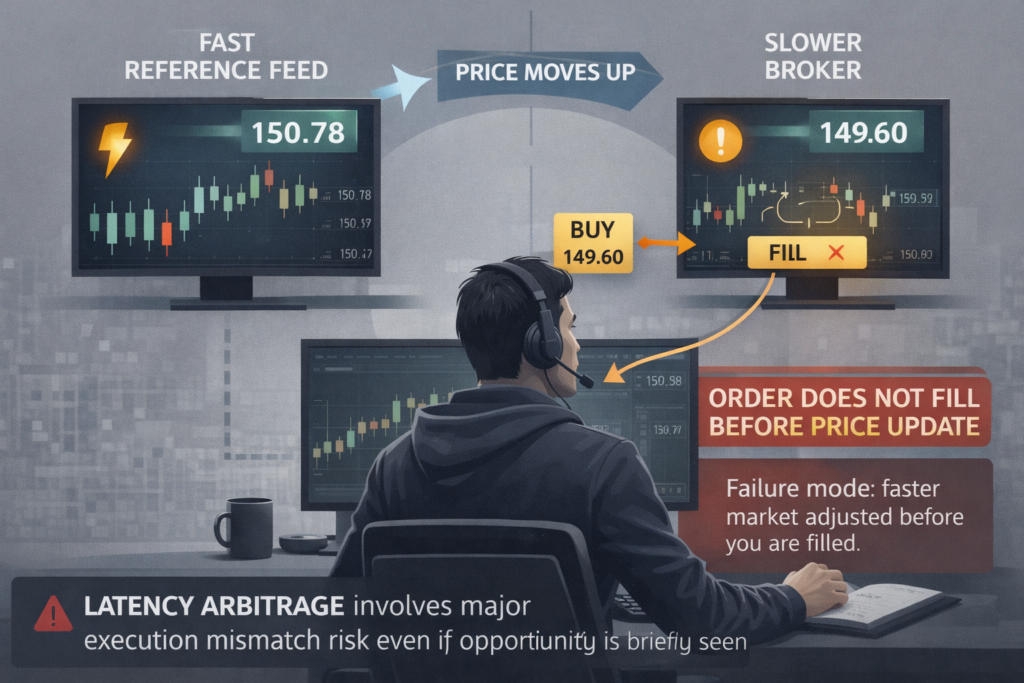

Latency arbitrage is an attempt to profit from the fact that the price has already “updated” somewhere, but has not yet updated elsewhere, allowing you to hit a stale quote. In the SharpTrader documentation, this is explicitly described as comparing prices between a “slow broker” and a fast price source (fast feed), and opening a trade when a discrepancy is detected.

3.2 Single-leg latency (1 leg): why it’s complicated for retail

Mechanics: You trade only on the “slow” side, hoping to get filled at an outdated price.

Why this scales poorly for retail:

-

the opportunity window is often microscopically short;

-

execution is not guaranteed;

-

costs (spread/slippage) easily eat up the “visible” profit;

-

in OTC/CFD environments, such patterns are often classified as undesirable.

There is also an important real-world layer here: many brokers explicitly prohibit latency arbitrage at the rules level and reserve the right to cancel or reject executions, or to restrict access. For example, in the educational materials of one popular broker, a latency arbitrage EA is explicitly listed as “not allowed.”

In their Order Execution Policy, there is also a clause granting the right to reject/cancel orders or restrict access if a client is involved in arbitrage, including latency and swap arbitrage.

Additionally, prop firms often explicitly include “arbitrage/latency trading” in their list of prohibited practices.

Conclusion on 1-leg latency: you might catch something occasionally, but as a sustainable business for retail, the odds are low—you are competing on speed and running into venue rules.

3.3 Two-leg latency (2 leg): “almost arbitrage,” but at a higher cost

Mechanics: you execute the first leg on the slow side and quickly hedge on the fast (or another slow) side, locking in the spread.

This sounds more “correct,” but new problems appear:

-

the risk that one leg is filled while the other is not, or is filled at a worse price;

-

doubled costs (commissions/spreads on two trades);

-

doubled infrastructure risks;

-

margin requirements on both sides.

And again, the execution environment matters. Broker risk systems and anti-fraud modules can detect “profitable trades opened during feed gaps” (price feed gaps) and treat them as latency exploitation. For example, Brokerpilot documentation describes a Latency Arbitrage trigger that flags such patterns.

Conclusion on 2-leg latency: the odds are slightly better than with 1-leg, but in mature markets and broker environments, retail is still playing on a field where infrastructure and flow status dominate.

4) Triangular arbitrage: why “three trades” often lose to “two layers of costs.”

4.1 The essence of the triangle

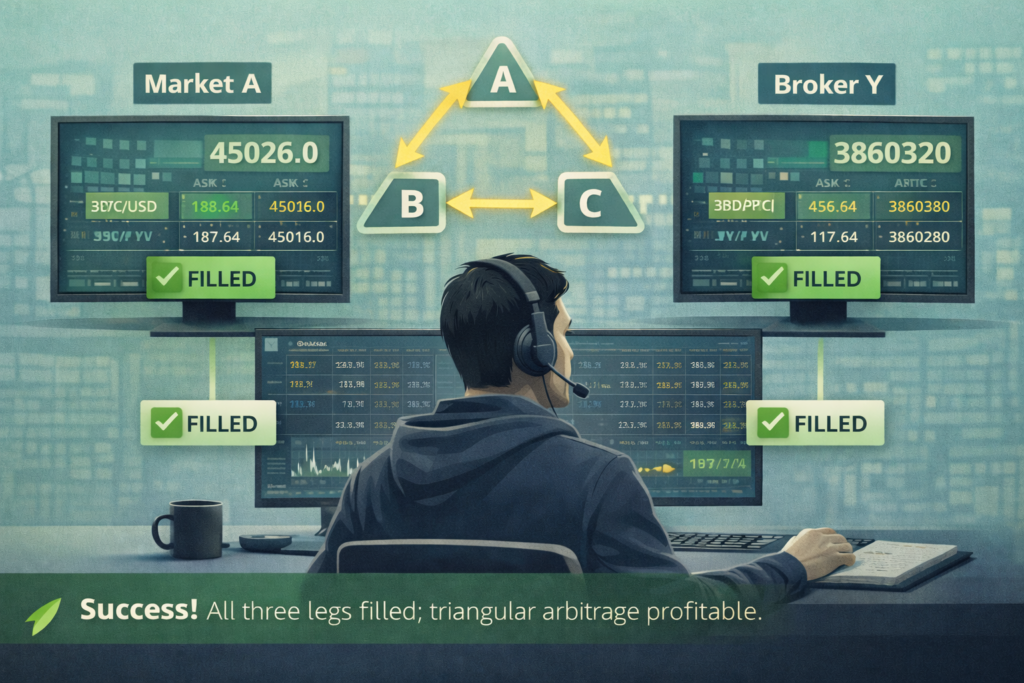

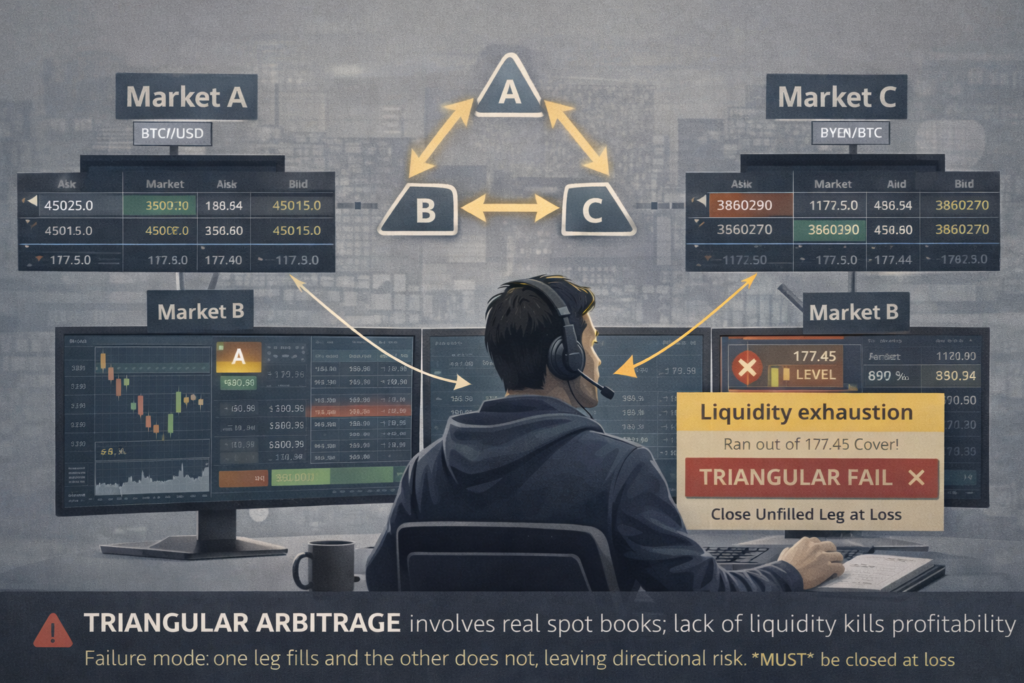

Triangular arbitrage exploits inconsistencies in cross rates: if A/B × B/C ≠ A/C (after accounting for commissions and spreads), you can execute a cycle of exchanges and return to the original currency with a profit.

In real trading, we distinguish:

-

intra-venue triangles (all three trades on one exchange / within one venue);

-

inter-venue triangles (legs on different venues), which in practice turn into a mix of latency plus settlement/transfer risks.

4.2 Why this is hard for retail

A triangle requires three executions, and any leg can:

-

be partially filled;

-

be filled at a worse price;

-

not be filled at all.

At the same time, you have at least three commissions. If you are a taker on each leg, mathematically, you often end up negative even when the loop looks “profitable” on paper.

4.3 Where the opportunity appears

Opportunities tend to arise more often:

-

in less liquid instruments;

-

during sharp market moves;

-

during technical desynchronizations.

But there is a paradox: the “fatter” the triangle looks, the more often it is a signal of poor liquidity, and slippage ends up eating it away.

Conclusion on triangular arbitrage: retail has a moderate chance if this is an intra-venue setup and if you truly know how to calculate costs and execute carefully. But as a “simple perpetual money machine”—no.

5) Two-leg and 3+ leg multi-leg lock arbitrage

Let’s be honest: there are reasons why these approaches can be mechanically more “survivable,” but automatically rating them 8/10 as a “chance to make money” is risky, because:

-

they often belong to the same latency family;

-

they add costs and complexity;

-

and “masking” is not alpha.

5.1 What the lock approach is

A lock approach is when the system holds two opposite positions (BUY and SELL) across different accounts or venues, and then “resolves” the divergence by closing, shifting, or reallocating part of the position.

The idea is to reduce the risk of “the first leg filled, the second didn’t,” because you already have a partially neutral structure, and management happens through closing/transferring/restructuring the legs.

5.2 Examples: LockCL2 and BrightTrio as implementations of multi-leg logic

In SharpTrader, these are described as a set of strategies grouped by a common logic core. In the Brief Strategies Overview, the following are explicitly listed:

-

Latency (1 leg),

-

Lock CL2 (2 accounts with opposite positions),

-

Lock CL3,

-

Bright Trio (3 accounts), and others.

The LockCL2 wiki also emphasizes that entry logic via closing/transferring positions makes the strategy “less directly associated” with latency arbitrage and helps it evade certain anti-arbitrage mechanisms for longer.

BrightTrio, on the other hand, is described on the wiki as latency arbitrage across three accounts with the goal of a “maximum masking effect.”

I intentionally will not expand this into a “how exactly to configure it to bypass detection” format. But from a trading analysis perspective, it can be summarized as follows:

Potential upside of multi-leg setups:

-

more degrees of freedom in leg management;

-

sometimes better tolerance to execution desynchronization.

The price of that upside:

-

higher commissions/spreads (more legs);

-

higher margin requirements;

-

more failure scenarios (one leg “stuck,” another “runs away,” a third doesn’t fill);

-

higher operational risk.

5.3 Why “multi-leg + masking” cannot automatically be treated as an “8/10 chance.”

Because two separate axes must be distinguished:

-

The trading axis: does the strategy have positive expected return after costs with acceptable risk?

-

The operational/legal axis: does the counterparty (broker/prop firm/exchange) allow this trading style, or will it be restricted by rules or risk systems?

If a strategy is built around exploiting delays, then even with good leg mechanics it remains in a zone where:

-

brokers may prohibit latency arbitrage and reserve the right to cancel/reject trades or restrict access;

-

prop firms may ban arbitrage/latency trading as a class;

-

risk providers for brokers build detectors for latency patterns.

So even if “masking” increases stealth, it is not equivalent to a guaranteed “chance to earn and withdraw.” In the real world, retail traders often lose not only on spread math, but also because the rules or the counterparty simply do not accept that type of risk.

6) PhantomDrift and Hybrid Masking: why “camouflage” =“the best arbitrage.

-

the highest odds are often attributed to strategies like PhantomDrift,

-

and even more so when combined with Hybrid Masking,

because of their high level of camouflage (including martingale elements and “resemblance to manual trading”).

I’ll integrate this into the article logically—as a separate layer: “operational trade-flow design”, but with important caveats.

6.1 How these strategies are described publicly

On the BJF Trading Group website, PhantomDrift is explicitly described as a hybrid of latency arbitrage and martingale (with a limited number of averaging steps), with the stated goal to “disguise arbitrage activity” and “confuse anti-arbitrage plugins.”

On the SharpTrader wiki, the Hybrid Masking Strategy is described as a mechanism to enhance the masking effect of arbitrage strategies within SharpTrader, and its linkage to PhantomDrift (activation/usage) is explicitly noted.

6.2 Why adding a martingale is not “free camouflage profit.”

The martingale component almost always:

-

increases tail risk (rare but potentially deep drawdowns);

-

can worsen risk-adjusted returns;

-

makes results more regime-dependent (trend regimes often “break” averaging logic, which is why a larger deposit is recommended compared to, say, LockCL2).

The goal is to make the trade profile less similar to a classic latency flow. But this does not guarantee robustness:

-

you become less predictable for filters,

-

but you pay for it with potential, though theoretically controllable, drawdowns.

6.3 The most important takeaway for the article

“High camouflage” is not the same as “high probability of profit.”

Camouflage is about how a strategy looks externally.

The probability of profit is about the expectancy after costs + risk control + the ability to operate legally and calmly with the chosen counterparty.

So in an honest article, it’s more correct to write not “PhantomDrift = 10/10,” but rather:

-

in marketing descriptions, PhantomDrift/Hybrid Masking are positioned as ways to alter the profile of arbitrage trades;

-

in real-world evaluation, one must consider that many counterparties prohibit latency-class strategies and reserve the right to cancel trades or restrict access;

-

and martingale elements can increase tail risks.

That’s why I’d rate PhantomDrift at 8/10.

I’ve never seen a 10/10—and I don’t think I ever will 😊

7) Hedged pairs / “pair trading”: where retail usually has a genuinely higher chance

Now we move to where retail traders more often find a sustainable edge: pair trading / relative value strategies.

7.1 The essence of the pair approach

You select two related assets, X and Y (economically or statistically), and construct a spread:

-

either a simple one (X − Y),

-

or with a hedge ratio (X − b·Y).

When the spread “moves too far,” you buy the “cheap” asset and sell the “expensive” one, expecting convergence.

7.2 Why the odds are higher here than in latency—and often higher than in triangular arbitrage

-

speed is not critical: positions can last minutes, hours, or days;

-

the edge often lies in discipline, not milliseconds;

-

costs are easier to control because you’re not hunting microsecond inefficiencies.

7.3 Risks that should not be glossed over

-

breakdown of the relationship (regime shift);

-

cost and availability of short selling;

-

impact of dividends/corporate actions (for stocks/ETFs);

-

risk of liquidity spread widening during stress regimes.

Conclusion on pairs: this is quasi-arbitrage, not risk-free. But it’s precisely here that retail traders can build a sustainable system with proper risk management.

8) Statistical arbitrage: an “umbrella” that can be both retail-friendly and fully institutional

Stat arb is not a single strategy but a family of approaches: from pairs to market-neutral baskets, factor long/short portfolios, and more.

8.1 Why “equity-style” stat arb is hard for retail to replicate

Because institutional stat arb typically requires:

-

large datasets and extensive data cleaning;

-

strict accounting for corporate actions;

-

very cheap execution;

-

scalable short selling;

-

portfolio optimization and exposure control.

8.2 Where stat arb becomes realistic for retail

-

longer horizons (hourly/daily), where costs are less destructive to the signal;

-

small baskets or pairs with clear economic intuition;

-

strict protection against overfitting (walk-forward analysis, out-of-sample tests, stress testing).

Conclusion on stat arb: retail does have a chance, but only if it does not try to copy HFT-style stat arb and instead builds a slower, more disciplined version.

9) An updated comparison of retail chances: one scale is no longer enough

To keep the article honest and non-promotional, I propose evaluating strategies along two dimensions:

-

Scale A: Trading feasibility (expectancy after costs + manageable risk)

-

Scale B: Operational survivability (rules, detection, counterparty, ability to operate calmly)

Because, for example, latency-based strategies may look profitable on demo or in tests, but run straight into broker/prop rules and risk systems.

9.1 Indicative ratings (for understanding the logic)

-

Latency 1 leg

-

A: 2–3/10 (costs and speed)

-

B: 0–3/10 (often restricted by rules/risk control)

-

-

Latency 2 leg

-

A: 3–4/10

-

B: 2–3/10 (for the same reasons)

-

-

Triangular

-

A: 3–5/10 (if intra-venue and costs are controlled)

-

B: 4–7/10 (usually less conflict with rules if it’s “normal” exchange mechanics)

-

-

Multi-leg lock (2 legs / lock approaches)

-

A: 5–6/10 (can be mechanically more robust, but more expensive and complex)

-

B: ~3/10 if it is essentially a latency family strategy in OTC/prop environments

-

-

Multi-leg lock (3+ legs / BrightTrio logic)

-

A: 6–7/10 (more flexibility, but also more costs and risks)

-

B: 3–4/10 in environments where arbitrage/latency practices are prohibited

-

-

Pairs / hedged relative value

-

A: 5–7/10 (with proper pair selection and cost control)

-

B: 6–9/10 (usually fewer conflicts if shorting/margin rules are respected)

-

-

Stat arb (on moderate horizons)

-

A: 4–7/10

-

B: 6–9/10

-

-

PhantomDrift + Hybrid Masking

-

A: 8/10

-

B: 9/10

-

Why I do not assign a universal “8/10” to multi-leg “masking” arbitrage: in real environments, these strategies often face bans or restrictions on arbitrage/latency-type practices, and “masking” does not eliminate costs, tail risks, or the counterparty’s rights under execution rules.

10) SharpTrader as “the tool.”

10.1 How SharpTrader is positioned

In the official SharpTrader wiki, it is described as a professional trading platform/workstation designed for advanced arbitrage across multiple markets (Forex, CFD, metals, futures, crypto), providing extended control and analytical capabilities.

10.2 Which strategies are publicly listed

On the SharpTrader Pro product page, the built-in/available strategies explicitly include:

-

Latency Arbitrage,

-

Lock / LockCL1 / LockCL2 / LockCL3,

-

PhantomDrift,

-

BrightDuo / BrightTrio,

-

Hedge Arbitrage,

-

Triangular Arbitrage,

-

Statistical Arbitrage,

and others.

In the Brief Strategies Overview on the wiki, strategies are additionally grouped as latency-based, hedge-based, and auxiliary, with BrightTrio, LockCL2, Statistical, etc., clearly listed there as well.

This means the statement “SharpTrader contains all the strategy types discussed in our article” can be supported by sources—with the clarification that some strategies are separate modules/options and not always “all included by default.”

10.3 Can it be called “the most professional”?

An absolute “the most” is always subjective. But we can honestly state the following:

-

SharpTrader is clearly positioned as a professional arbitrage platform (according to the manufacturer’s description/wiki).

-

Some reviews describe SharpTrader as “the most professional” among commercially available arbitrage programs for Forex and crypto and give it high ratings—but that is the opinion of specific reviewers, not an objective “market fact.”

Framed this way, the conclusion is coherent, balanced, and verifiable.

Comparative Evaluation of Arbitrage Strategies for Retail Traders

Scoring scale:

-

1 = very low

-

10 = very high

Scores reflect practical reality for retail traders, not theoretical arbitrage.

| Strategy Type | Capital Efficiency | Technical Complexity | Execution Risk | Scalability | Broker / Venue Compatibility | Retail Success Probability |

|---|---|---|---|---|---|---|

| 1-Leg Latency Arbitrage | 4/10 | 6/10 | 9/10 | 2/10 | 1/10 | 1/10 |

| 2-Leg Latency Arbitrage | 5/10 | 7/10 | 8/10 | 3/10 | 2/10 | 2/10 |

| Triangular Arbitrage | 6/10 | 6/10 | 7/10 | 4/10 | 6/10 | 4/10 |

| Hedged Pair Trading (Relative Value) | 7/10 | 6/10 | 5/10 | 6/10 | 8/10 | 6/10 |

| Statistical Arbitrage (Retail-Scale) | 6/10 | 7/10 | 6/10 | 6/10 | 7/10 | 6/10 |

| 2-Leg Lock Arbitrage (LockCL-type) | 6/10 | 8/10 | 6/10 | 5/10 | 3/10 | 5/10 |

| 3+-Leg Lock Arbitrage (BrightTrio-type) | 6/10 | 9/10 | 6/10 | 6/10 | 3/10 | 6/10 |

| Latency + Lock (Multi-Leg Hybrid) | 5/10 | 9/10 | 7/10 | 5/10 | 2/10 | 5/10 |

| PhantomDrift-type Hybrid (Latency + RV) | 6/10 | 8/10 | 6/10 | 6/10 | 5/10 | 7/10 |

| PhantomDrift + Hybrid Masking | 6/10 | 9/10 | 3/10 | 6/10 | 6/10 | 8/10 |

How to Read This Table

Key Columns Explained

-

Capital Efficiency

How effectively capital is used relative to margin and lock requirements. -

Technical Complexity

Infrastructure, logic, monitoring, and failure-handling difficulty. -

Execution Risk

Risk of partial fills, slippage, leg mismatch, and timing failure. -

Scalability

Ability to increase volume without destroying edge. -

Broker / Venue Compatibility

Likelihood that the strategy is allowed and can operate long-term without intervention. -

Retail Success Probability

Overall risk-adjusted probability of sustainable profitability for retail traders.

11) Practical checklist: how retail can realistically improve the odds (no magic, no “bypasses”)

So the article doesn’t remain purely theoretical, here’s a checklist that applies equally to triangular, pairs, and stat arb—and partially to multi-leg setups:

-

Calculate all-in costs

-

commissions, spreads, slippage, swaps/funding, cost of capital.

-

-

Model leg break scenarios

-

what if one leg fills and the other doesn’t?

-

what if it fills partially?

-

what if connectivity/API fails?

-

-

Check liquidity and scalability

-

if your “opportunity” disappears at 0.5–1 lot, it’s not a strategy—it’s a micro anomaly.

-

-

Test robustness

-

out-of-sample testing,

-

stress regimes (news/volatility),

-

spread widening.

-

-

Read counterparty rules

-

especially when trading via brokers or prop firms: bans on arbitrage/latency/HFT are often explicitly stated in the rules.

-

12) Final conclusion: does retail have a chance in arbitrage?

Yes—there is a chance, but it is unevenly distributed.

-

In latency arbitrage (and its multi-leg lock variations, if the core remains latency-dependent), retail’s odds are limited by infrastructure, costs, and often by broker/prop firm rules and detection.

-

In triangular arbitrage, opportunities do exist, but they are often eaten away by three executions and costs; in practice, it works as a niche mechanic rather than a money-printing machine.

-

The most realistic long-term opportunities for retail more often lie in pairs/relative value strategies and moderate stat arb on longer horizons, where competition is less about microseconds and the edge can be built through models, discipline, and risk management.

-

The highest odds, in my view, are currently in PhantomDrift and in next-generation strategies with masking that resemble “inexperienced retail trading,” allowing them to pass broker and prop-firm filters more effectively.

Frequently Asked Questions (FAQ)

Does retail trading actually have a chance in arbitrage?

Yes. Retail traders do have a chance in arbitrage—but not evenly across all strategy types. The key is choosing approaches where the edge comes from structure, trade-flow design, and risk management, rather than pure speed or infrastructure.

Why is classic latency arbitrage so difficult for retail traders?

Classic one-leg or two-leg latency arbitrage relies heavily on:

-

execution speed,

-

ultra-low costs,

-

and privileged infrastructure.

In modern broker and prop-firm environments, these factors strongly favor institutional players. Retail traders are often constrained not only by latency, but also by execution rules and risk controls.

Does that mean latency arbitrage is completely unusable for retail?

Not necessarily.

While pure latency arbitrage is challenging, advanced implementations that redesign the trade-flow profile can significantly improve practical usability for retail traders.

This is where strategies like PhantomDrift and Hybrid Masking come into play.

What makes PhantomDrift different from classic arbitrage?

PhantomDrift is not just a latency strategy—it is a hybrid execution framework.

Its key idea is not to chase raw speed, but to:

-

reshape the execution pattern,

-

reduce the visual footprint of classic arbitrage,

-

and distribute risk more dynamically.

This shifts the strategy from “speed competition” toward operational robustness.

Why is Hybrid Masking important?

Hybrid Masking adds an additional layer of trade-flow normalization.

Instead of trades looking like a rigid arbitrage pattern, the strategy:

-

produces a more diversified execution structure,

-

blends arbitrage logic with non-linear position behavior,

-

and results in a trade profile that looks closer to discretionary or mixed-style trading.

This improves operational survivability without changing the underlying market logic.

Does “masking” mean bypassing broker rules?

No.

Masking is not about bypassing rules—it is about how a strategy behaves structurally.

Every broker and prop firm evaluates patterns, not intentions.

A strategy that:

-

manages positions gradually,

-

avoids mechanical spikes,

-

and behaves consistently across regimes

is inherently more compatible with modern risk systems.

Isn’t adding a martingale risky?

Martingale elements always increase risk if misused.

However, in PhantomDrift they are:

-

limited,

-

controlled,

-

and used as a trade-flow smoothing mechanism, not as an aggressive recovery.

When applied correctly, this can improve risk distribution rather than amplify it.

Why do PhantomDrift + Hybrid Masking score higher than other arbitrage approaches?

Because they perform well on both critical dimensions:

-

Trading feasibility

-

robust execution logic,

-

positive expectancy after costs,

-

adaptability to different market conditions.

-

-

Operational survivability

-

lower conflict with broker risk systems,

-

reduced dependency on microsecond advantages,

-

better long-term account stability.

-

Very few arbitrage frameworks address both dimensions simultaneously.

Are PhantomDrift and Hybrid Masking suitable for beginners?

They are not beginner-level strategies, but retail-accessible professional strategies.

They are best suited for traders who:

-

understand risk,

-

value consistency over hype,

-

and prefer long-term survivability over short-term spikes.

How do these strategies compare to pairs or statistical arbitrage?

Pairs and stat arb are excellent long-term approaches, especially on slower horizons.

PhantomDrift and Hybrid Masking differ in that they:

-

operate closer to execution mechanics,

-

adapt dynamically to microstructure,

-

and can function in environments where classic arbitrage would fail.

They complement, rather than replace, relative-value strategies.

Is PhantomDrift a “guaranteed” strategy?

No serious strategy is ever guaranteed.

What PhantomDrift offers is:

-

a higher-quality risk profile,

-

better execution survivability,

-

and a more realistic path for retail traders operating in modern markets.

That’s why it consistently ranks near the top in practical evaluations.

Why is a 10/10 rating unrealistic for any arbitrage strategy?

Because markets evolve, rules change, and risk is never zero.

A strategy rated 8/10 that:

-

survives,

-

adapts,

-

and compounds steadily

is far more valuable than a hypothetical 10/10 that fails operationally.

What is the main takeaway of the article?

Retail arbitrage is not dead, but it requires a different mindset.

The future belongs to strategies that:

-

combine arbitrage logic with intelligent execution,

-

respect operational realities,

-

and prioritize survivability over theoretical purity.

PhantomDrift + Hybrid Masking represent exactly this next step.