English

English Deutsch

Deutsch 日本語

日本語 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

التنقل في عالم المراجحة: مراجحة التأخير الزمني، والمقفلة، والتحوط، والثلاثية، والإحصائية – دليل شامل لاختيار الأنسب لك 15/06/2023 – Posted in: Arbitrage Software, cryptoarbitrage software, Forex trading

المراجحة (Arbitrage)، وهو مصطلح مشتق من الكلمة الفرنسية arbitrer التي تعني «الحُكم»، يشير إلى الشراء والبيع المتزامن لأصل مالي بهدف تحقيق ربح من فروقات الأسعار بين الأسواق المختلفة. تنشأ هذه الفروقات نتيجة لاختلالات العرض والطلب، والعوامل الجيو-اقتصادية، وفجوات المعلومات. وعلى الرغم من أن جميع استراتيجيات المراجحة تسعى إلى الاستفادة من هذه الاختلافات السعرية، إلا أن طرق التنفيذ تختلف اختلافًا كبيرًا.

لننطلق في جولة داخل عالم المراجحة ونتعرّف على خمسة أنواع مختلفة: مراجحة التأخير الزمني (Latency)، والمراجحة المقفلة (Lock)، ومراجحة التحوط (Hedge)، والمراجحة الثلاثية (Triangular)، والمراجحة الإحصائية (Statistical). يتمتع كل نوع بتحدياته ومكافآته الخاصة، وفهم هذه الفروقات هو المفتاح لاختيار الاستراتيجية التي تتناسب مع مستوى تقبّل المخاطر لديك، ومهاراتك، وأهدافك الاستثمارية.

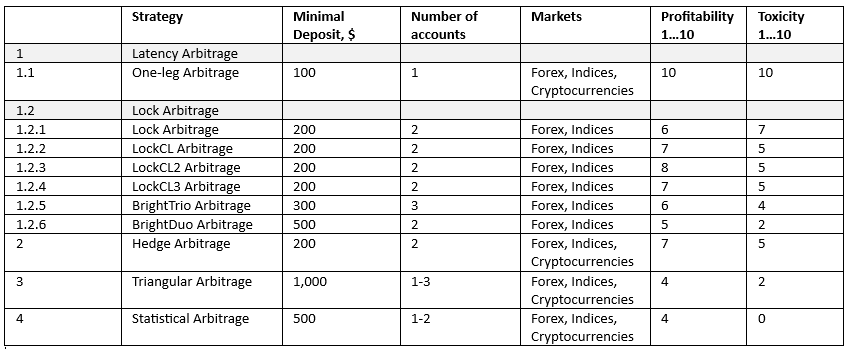

مراجحة التأخير الزمني (Latency Arbitrage)

1.1 استراتيجية المراجحة أحادية الجانب (One-Leg Arbitrage)

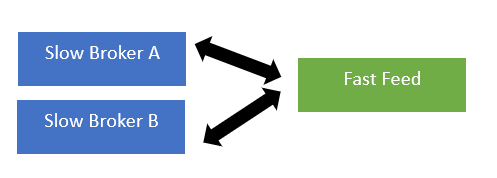

تعتمد استراتيجية المراجحة أحادية الجانب على استغلال فروقات التأخير الزمني، لا سيما في التداول عالي التردد (HFT). يستخدم المتداولون تقنيات متقدمة للتنبؤ بفروقات الأسعار بين الأسواق الناتجة عن بطء انتقال المعلومات. وعلى الرغم من قدرتها على تحقيق أرباح سريعة وكبيرة، إلا أنها تتطلب استثمارات تقنية مرتفعة وتتميز بمنافسة شديدة بين شركات التداول عالي التردد.

في هذا النوع من المراجحة، يقوم برنامج المراجحة بمقارنة الأسعار في حساب يُعرف بـ«الحساب البطيء» مع مصدر أسعار سريع يُسمى «التغذية السريعة». إذا سبق سعر التغذية السريعة سعر الحساب، يفتح البرنامج أمر شراء على الحساب البطيء، والعكس صحيح.

إذا كنت تمتلك رأس مال كبيرًا، وخبرة تقنية متقدمة، واستعدادًا لتحمل مخاطر عالية، فقد تكون مراجحة التأخير الزمني خيارًا مناسبًا لك.

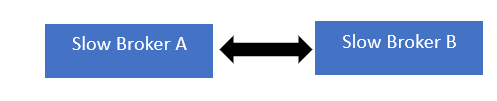

1.2 المراجحة المقفلة (Lock Arbitrage)

تُعد المراجحة المقفلة نوعًا آخر من مراجحة التأخير الزمني، حيث تتم مقارنة أسعار التغذية السريعة مع حسابين بطيئين. الهدف هو قفل الأرباح أو التحوط والحفاظ على الصفقة مفتوحة لأطول فترة ممكنة.

تتضمن المراجحة المقفلة شراء وبيع نفس الأداة المالية في أسواق مختلفة في الوقت نفسه لتحقيق ربح مضمون من فروق الأسعار. وتُعتبر هذه الاستراتيجية منخفضة المخاطر نسبيًا، لأن الصفقات تعوض بعضها البعض، لكنها تتطلب مراقبة مستمرة وتبقى عرضة لمخاطر التنفيذ.

1.2.1 استراتيجية Lock Arbitrage

تتيح هذه التقنية للبرنامج قفل الأرباح في أسرع وقت ممكن أو عند أصغر فرق نقاط (Pips). يتم فتح أمر شراء وأمر بيع متعاكسين على حسابين مختلفين. عند ظهور فرصة مراجحة، يتم إكمال الصفقة وربط أمر افتراضي مطابق بأمر وقف متحرك.

1.2.2 استراتيجية LockCL

تشبه هذه الاستراتيجية طريقة Lock، لكنها تمكّن البرنامج من تأمين الأرباح على الحساب نفسه دون إغلاق الصفقة، مع انتظار فرصة المراجحة التالية باستخدام أوامر افتراضية.

1.2.3 استراتيجية LockCL2

تعتمد هذه الاستراتيجية على منطق مشابه، لكن مع اختلاف في طريقة إعادة فتح الأوامر بعد تحقق شروط الإغلاق.

1.2.4 استراتيجية LockCL3

صُممت هذه التقنية لتنفيذ المراجحة على حساب واحد، بينما يُستخدم الحساب الآخر لأغراض القفل فقط.

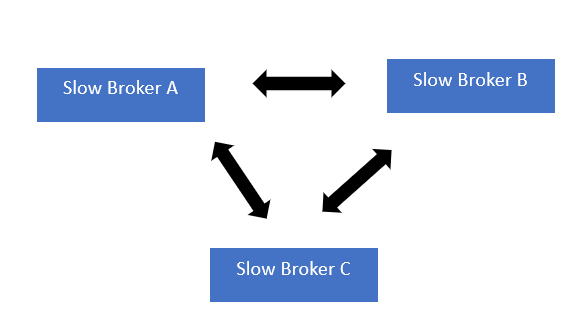

1.2.5 استراتيجية BrightTrio

BrightTrio هي استراتيجية متقدمة مصممة للتداول عبر ثلاثة حسابات (A وB وC)، وتهدف إلى تعظيم الأرباح مع إخفاء أنشطة المراجحة بفعالية.

1.2.6 استراتيجية BrightDuo

تتميز BrightDuo بخوارزمية شديدة التعقيد، وسيتم شرحها بالتفصيل في هذا المقال.

إذا كنت تفضل استراتيجية استثمارية أكثر تحفظًا ولديك القدرة على مراقبة الأسواق باستمرار، فقد تكون المراجحة المقفلة مناسبة لك.

استراتيجية مراجحة التحوط (Hedge Arbitrage)

مراجحة التحوط، المعروفة أيضًا باسم تداول الأزواج، تتضمن فتح صفقة شراء على أصل وصفقة بيع على أصل مرتبط به. تعتمد هذه الاستراتيجية على الارتباط الإحصائي بين الأداتين وتهدف إلى الاستفادة من أي انحراف عن هذا الارتباط، مع تقليل المخاطر من خلال تعويض الخسائر المحتملة.

إذا كنت تمتلك فهمًا جيدًا للتحليل الإحصائي ومستعدًا لتحمل مستوى متوسط من المخاطر، فقد تكون مراجحة التحوط خيارك المناسب.

استراتيجية المراجحة الثلاثية (Triangular Arbitrage)

تتضمن المراجحة الثلاثية التداول بثلاث عملات مختلفة في ثلاثة أسواق مختلفة. يتم تحقيق الأرباح من خلال استغلال فروقات أسعار الصرف بين هذه العملات. تُعد هذه الاستراتيجية معقدة وتتطلب مراقبة مستمرة، وغالبًا ما تُنفذ عبر أنظمة تداول خوارزمية.

إذا كنت متمرسًا في أسواق الفوركس وتمتلك الموارد اللازمة للتداول الخوارزمي، فقد تكون المراجحة الثلاثية خيارًا مناسبًا لك.

استراتيجية المراجحة الإحصائية

تعتمد المراجحة الإحصائية على النمذجة الرياضية لتحديد فرص التداول بناءً على البيانات التاريخية والعوامل السوقية المختلفة. ورغم أنها قد تكون مربحة للغاية، إلا أنها تتطلب فهمًا عميقًا للتحليل الكمي والنماذج الرياضية.

الخلاصة

يعتمد اختيار استراتيجية المراجحة المناسبة على أهدافك المالية ومستوى المخاطرة الذي تتحمله ومهاراتك. لكل استراتيجية توازنها الخاص بين المخاطر والعوائد ومتطلباتها التقنية.

التعريف بـ SharpTrader™: برنامج المراجحة المتكامل للتداول المتقدم

يمنحك SharpTrader™ القدرة على استغلال عدم كفاءة الأسواق بدقة وسرعة، مع مجموعة واسعة من استراتيجيات المراجحة وواجهة استخدام سهلة تناسب المبتدئين والمحترفين على حد سواء.