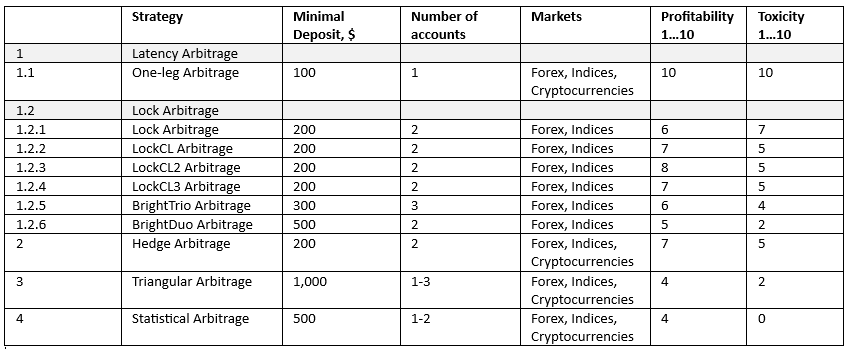

English

English 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

Navigation durch die Welt der Arbitrage: Latenz-, Lock-, Hedge-, Dreiecks- und statistische Arbitrage – Ein umfassender Leitfaden zur Wahl der besten Strategie für Sie Donnerstag, der 15. Juni 2023 – Posted in: Arbitrage Software, cryptoarbitrage software, Forex trading

Arbitrage, ein Begriff, der vom französischen Wort „arbitrer“ (urteilen) abgeleitet ist, bezeichnet den gleichzeitigen Kauf und Verkauf eines Vermögenswertes, um von Preisunterschieden auf verschiedenen Märkten zu profitieren. Diese Ungleichgewichte entstehen durch Unterschiede in Angebot und Nachfrage, geoökonomische Faktoren sowie Informationsasymmetrien. Während alle Arbitrage-Strategien darauf abzielen, solche Preisabweichungen auszunutzen, unterscheiden sich die Methoden teilweise erheblich.

Begeben wir uns auf eine Reise durch die Welt der Arbitrage und betrachten fünf verschiedene Typen – Latenz-, Lock-, Hedge-, Dreiecks- und statistische Arbitrage. Jede dieser Strategien bringt eigene Herausforderungen und Chancen mit sich. Das Verständnis dieser Unterschiede ist entscheidend, um die Strategie zu wählen, die am besten zu Ihrer Risikobereitschaft, Ihrem Kenntnisstand und Ihren Anlagezielen passt.

Latenz-Arbitrage

1.1 One-Leg-Arbitrage-Strategie

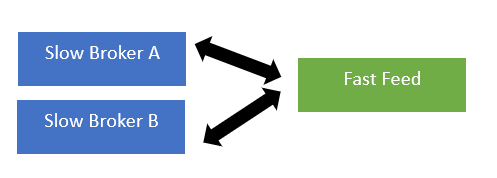

Die One-Leg-Arbitrage nutzt Zeitverzögerungen, insbesondere im High-Frequency-Trading (HFT). Trader setzen modernste Technologien ein, um Preisabweichungen zwischen Märkten auszunutzen, die durch Verzögerungen bei der Informationsübertragung entstehen. Obwohl diese Methode schnelle und teils erhebliche Gewinne ermöglichen kann, erfordert sie hohe Anfangsinvestitionen in Technologie und ist durch starken Wettbewerb zwischen HFT-Firmen geprägt.

Bei der One-Leg-Arbitrage vergleicht die Arbitrage-Software Kurse eines sogenannten „langsamen Kontos“ mit einer schnellen Kursquelle, dem „Fast Feed“. Liegt der Fast-Feed-Preis vor dem Kontopreis, eröffnet das Programm eine Kauforder auf dem langsamen Konto – und umgekehrt.

Wenn Sie über erhebliches Kapital, die erforderliche technologische Expertise und eine hohe Risikobereitschaft verfügen, kann Latenz-Arbitrage eine geeignete Wahl sein.

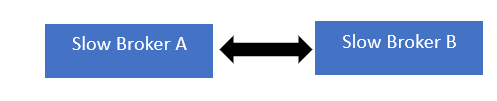

1.2 Lock-Arbitrage

Der Lock-Arbitrage-Algorithmus ist ebenfalls eine Form der Latenz-Arbitrage, bei der Fast-Feed-Kurse mit zwei langsamen Konten verglichen werden. Ziel ist es, Gewinne durch Hedging oder „Locking“ möglichst lange zu sichern.

Lock-Arbitrage bedeutet den gleichzeitigen Kauf und Verkauf desselben Instruments auf verschiedenen Märkten, um einen garantierten Gewinn aus Preisunterschieden zu sichern. Das Risiko ist vergleichsweise gering, da sich die beiden Positionen gegenseitig absichern. Allerdings erfordert diese Strategie eine kontinuierliche Überwachung und ist anfällig für Ausführungsrisiken.

1.2.1 Lock-Arbitrage-Strategie

Diese Technik ermöglicht es der Software, Gewinne entweder in kürzester Zeit oder bei minimaler Pip-Differenz zu sichern. Dabei werden zwei entgegengesetzte Orders (Kauf und Verkauf) auf zwei unterschiedlichen Konten platziert. Sobald eine Arbitrage-Gelegenheit entsteht, wird die Order abgeschlossen und die entsprechende virtuelle Order mit Trailing Stop versehen.

1.2.2 LockCL-Arbitrage-Strategie

Diese Variante erlaubt es, Gewinne auf demselben Konto zu sichern, ohne den Trade direkt zu schließen. Stattdessen wird auf die nächste Arbitrage-Gelegenheit gewartet, wobei virtuelle Orders mit SL, TP und Trailing Stop verwendet werden.

1.2.3 LockCL2-Arbitrage-Strategie

Ähnlich wie LockCL, jedoch mit umgekehrter Logik bei der Wiedereröffnung der Positionen nach dem Erreichen der definierten Bedingungen.

1.2.4 LockCL3-Arbitrage-Strategie

Diese Technik führt Arbitrage auf einem Konto aus, während ein anderes ausschließlich zum Locking genutzt wird.

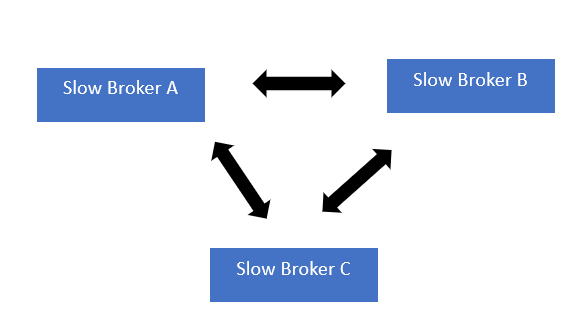

1.2.5 BrightTrio-Arbitrage-Strategie

BrightTrio ist eine spezialisierte Strategie für den Handel über drei Konten (A, B und C), die darauf ausgelegt ist, Arbitrage-Trades effektiv zu verschleiern und gleichzeitig Gewinne zu maximieren.

1.2.6 BrightDuo-Arbitrage-Strategie

Die BrightDuo-Strategie basiert auf einem äußerst komplexen Algorithmus und wird detailliert in diesem Artikel beschrieben.

Wenn Sie eine konservativere Anlagestrategie bevorzugen und die Märkte kontinuierlich überwachen können, ist Lock-Arbitrage möglicherweise die richtige Wahl.

Hedge-Arbitrage-Strategie

Hedge-Arbitrage, auch als Pair Trading bekannt, beinhaltet eine Long-Position in einem Wertpapier und eine Short-Position in einem verwandten Wertpapier. Ziel ist es, Abweichungen von der statistischen Korrelation auszunutzen, wobei Verluste einer Position durch Gewinne der anderen ausgeglichen werden können.

Wenn Sie über solide statistische Kenntnisse verfügen und ein moderates Risiko eingehen möchten, könnte Hedge-Arbitrage gut zu Ihnen passen.

Dreiecks-Arbitrage-Strategie

Die Dreiecks-Arbitrage umfasst den Handel mit drei verschiedenen Währungen auf drei Märkten. Gewinne entstehen durch Ausnutzung von Wechselkursabweichungen. Diese Strategie ist komplex und wird meist von algorithmischen Systemen umgesetzt.

Wenn Sie über fundierte Forex-Kenntnisse und die nötigen Ressourcen für algorithmischen Handel verfügen, könnte Dreiecks-Arbitrage die richtige Wahl sein.

Statistische Arbitrage-Strategie

Die statistische Arbitrage nutzt mathematische Modelle, um Handelschancen zu identifizieren. Sie erfordert tiefgehende quantitative Kenntnisse, kann jedoch äußerst profitabel sein.

Fazit

Die Wahl der richtigen Arbitrage-Strategie hängt von Ihren finanziellen Zielen, Ihrer Risikobereitschaft und Ihren Fähigkeiten ab. Jede Strategie bringt eigene Chancen und Risiken mit sich.

SharpTrader™ – Die ultimative Arbitrage-Software

SharpTrader™ revolutioniert den Arbitrage-Handel durch modernste Technologie, vielfältige Strategien und eine benutzerfreundliche Oberfläche. Nutzen Sie Marktineffizienzen effizient und verschaffen Sie sich einen echten Wettbewerbsvorteil.

SharpTrader™ jetzt kaufen und die Zukunft des Tradings erleben!