Deutsch

Deutsch 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

The Evolution of Arbitrage Trading in 2026: From Infrastructure Arms Race to Intelligent Flow Masking Thursday March 26th, 2026 – Posted in: Arbitrage Software – Tags: AI order flow analysis, anti-arbitrage detection, anti-arbitrage detection bypass, arbitrage trading 2026, forex latency arbitrage, HFT obfuscation, Hybrid Masking strategy, intelligent order flow masking, latency arbitrage masking, order flow camouflage, PhantomDrift strategy, sharptrader, toxicity scoring

Abstract

This paper examines the structural transformation of arbitrage trading through 2026, with a particular focus on the shift from infrastructure-based competitive advantage to intelligent order-flow masking. While colocation, low-latency data feeds, and hardware acceleration remain necessary prerequisites, they no longer constitute differentiating factors in a market where AI-powered broker-side detection systems can identify and penalize informed flow in real time. Drawing on published commercial implementations — including the Phantom Drift strategy and the Hybrid Masking (MA + Fibonacci) framework developed by BJF Trading Group — the paper analyzes how modern arbitrageurs must generate statistically plausible, behaviorally camouflaged order flow to preserve access to competitive liquidity. Regulatory and ethical dimensions are also addressed.

1. Introduction

For several decades, arbitrage trading on financial markets has been governed by a single foundational principle: whoever detects and exploits price inefficiencies first, profits. This principle gave rise to the high-frequency trading (HFT) industry, in which competitive advantage was measured in nanoseconds and infrastructure investments ran into hundreds of millions of dollars. Physical proximity to matching engines, market data feed quality, and bandwidth capacity were — and remain — the necessary entry conditions.

By 2026, however, the competitive landscape of arbitrage trading has undergone a qualitative transformation that cannot be described merely as another cycle of the technological arms race. The deployment of real-time AI analytics systems by brokers, market makers, and liquidity providers (LPs) has made arbitrage activity automatically identifiable with unprecedented accuracy. Mathematically perfect order flow — the very ideal toward which every algorithmic trader strived — has become a toxicity marker. The paradox is stark: excessively efficient trading is now penalized through restricted access to liquidity.

This paper examines three interconnected phenomena: first, the transformation of the role of infrastructure factors in modern arbitrage; second, the mechanics of AI-based order flow detection and its consequences for market participants; and third, the emergence of a new class of techniques — intelligent flow masking — which is becoming the key differentiator in the competitive environment of 2026. The paper also addresses the regulatory and ethical dimensions of these practices, as the boundary between legitimate obfuscation and market manipulation remains a subject of active debate.

2. Classical Competitiveness Factors: Necessary Conditions That Lost Their Differentiating Power

2.1 Colocation and Physical Proximity to the Matching Engine

The concept of colocation — placing trading servers in immediate proximity to the exchange matching engine — became an industry standard in the late 2000s. The logic is straightforward: the speed of light is finite, and every meter of cable adds latency. The world’s major exchanges — NYSE, CME, Eurex — offer colocation services as commercial products, thereby standardizing access to minimum latency for all participants willing to pay the relevant fees.

By the mid-2010s, competition in this domain had reached physical limits: intra-datacenter latencies were measured in single-digit microseconds, and further reductions required transitioning to fundamentally different technological solutions — fiber-optic links yielding to microwave and even laser communication between trading venues. The infrastructure linking Chicago and New York serves as an illustrative example: microwave towers achieve data transmission in approximately 4.09 milliseconds versus 6.65 milliseconds via fiber — a difference critical for inter-exchange arbitrage between CME and NYSE.

Yet by 2026, colocation had ceased to be a source of sustainable competitive advantage for a simple reason: it had become available to all serious market participants. The barrier to entry fell, and the uniformity of infrastructure among top HFT firms means that any one player’s gain at the physical placement level is automatically neutralized by equivalent investments from competitors.

2.2 Market Data Feed Quality and Latency Arbitrage

The market data feed — the stream of prices, volumes, and order book states — is the second classical competitiveness factor. The gap between a direct exchange feed and a consolidated aggregated feed can range from several microseconds to several milliseconds: sufficient to construct an entire trading strategy based on information advantage.

Latency arbitrage in the classical sense exploits precisely this asymmetry: a trader receiving a price update faster than competitors can execute a trade at a stale quote before it is corrected. Regulators have repeatedly drawn attention to this practice — the SEC, in particular, has characterized it in its reports as potentially unfair to retail investors — yet it remains legal in most jurisdictions, provided disclosure requirements are met.

By 2026, the quality of direct feeds had also been substantially standardized among professional participants. The emergence of normalized feeds with guaranteed latency parameters (deterministic latency) from leading market data providers further eroded the advantages associated with differentiated information access.

2.3 Hardware Acceleration: FPGAs and Kernel Bypass

Alongside the infrastructure race, hardware solutions for order processing acceleration have matured. Field-Programmable Gate Arrays (FPGAs) enable logic to be implemented directly at the hardware level, bypassing the operating system and achieving latencies in the single-digit nanosecond range. Kernel bypass technologies — DPDK (Data Plane Development Kit) and RDMA (Remote Direct Memory Access) — enable direct data transfer between the network card and application memory, eliminating OS kernel overhead.

This combination of technologies created a class of participants capable of reacting to market events faster than any software solution. Yet here too, competition produced capability convergence: leading HFT firms employ similar technology stacks, and the performance gap between them is decreasingly determined by hardware and increasingly by algorithm quality and — crucially — the ability to avoid identification.

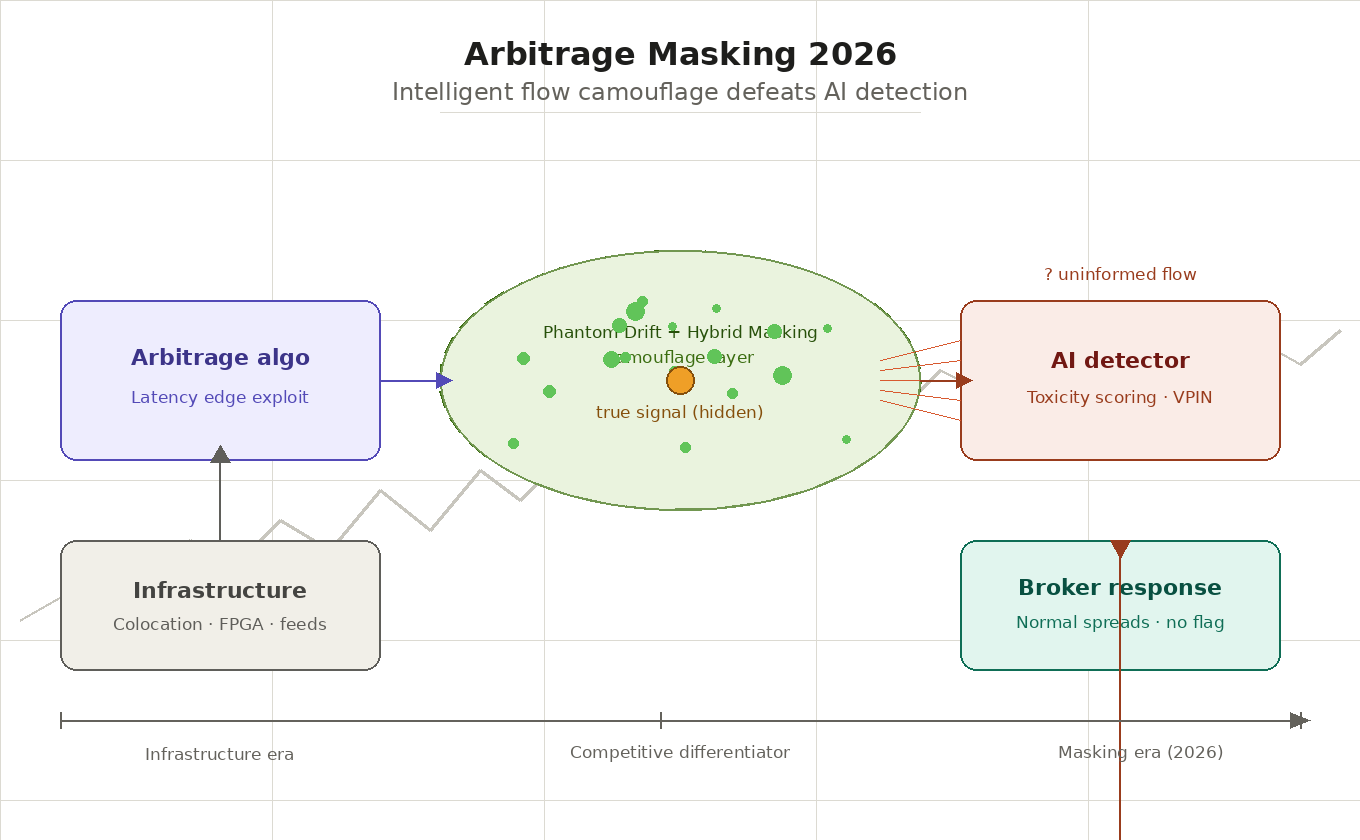

Thus, by 2026, infrastructure factors constitute a necessary but insufficient foundation for arbitrage activity. They answer the question of whether you can trade, but not the question of whether you will be permitted to trade — and it is precisely the second question that has become central to modern practice.

3. AI Detection and Flow Toxicity: The New Threat to Arbitrageurs

3.1 The Emergence of Real-Time Analytics Systems on the Counterparty Side

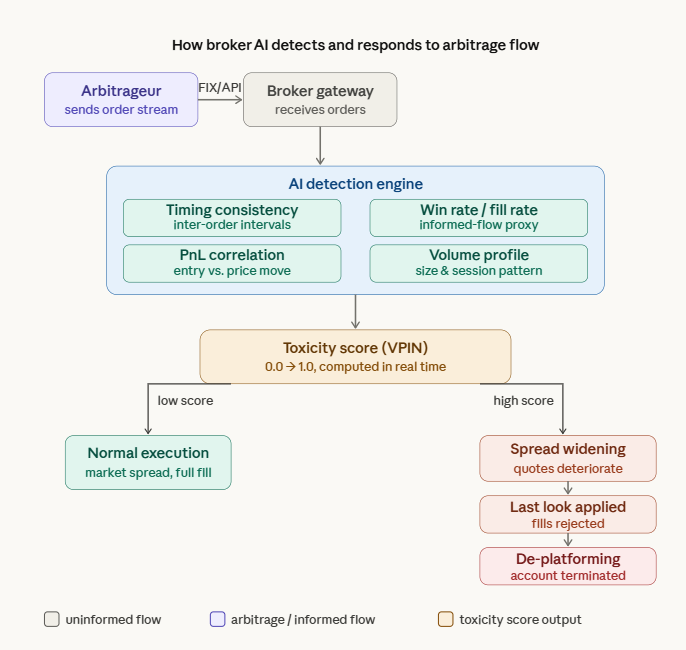

The proliferation of machine learning and the accessibility of high-performance computing led, by the mid-2020s, to the largest brokers, market makers, and ECNs (Electronic Communication Networks) deploying proprietary AI systems for real-time analysis of client order flow. Such systems are positioned by market participants as risk-management and liquidity-optimization tools — yet they function as detectors of “toxic” clients: those whose trading is systematically unprofitable for the liquidity provider due to information asymmetry.

These systems analyze a multitude of variables within a rolling time window: fill rate, timing consistency, the ratio of winning to losing trades, correlation between entry points and subsequent price movements, volume profiles, and intraday activity distributions. The combination of these metrics enables high-accuracy separation of informed flow — order flow carrying information about future price movements — from uninformed flow generated by retail participants.

3.2 The Concept of Toxicity Scoring and Adverse Selection

The concept of order flow “toxicity” originates in the academic literature on market microstructure. The foundational work of Glosten and Harris (1988) established the theoretical basis for decomposing the bid-ask spread into informational and operational components. This concept was subsequently operationalized through the VPIN metric (Volume-synchronized Probability of Informed Trading), proposed by Easley, Lopez de Prado, and O’Hara in 2011, which assesses the probability that a counterparty holds an information advantage.

In practical applications, the toxicity score is a dynamically updated indicator that reflects the probability that a given client trades on information unavailable to the market maker. A high value implies that every transaction with that client is, on average, loss-making for the liquidity provider due to adverse selection — the phenomenon whereby one party to a trade systematically loses to the other as a result of information asymmetry.

3.3 Consequences of a High Toxicity Score: From Spread Widening to De-Platforming

The response of brokers and LPs to a client’s elevated toxicity score unfolds through several mechanisms of varying severity. At the first level: dynamic spread widening — the market maker automatically deteriorates quotes for identified arbitrageurs, making their strategy unprofitable without an outright service refusal. The second level: last look — the LP’s right to reject an order even after receipt, if the quote has moved adversely during processing. The third level: explicit restrictions — limits on volume, order frequency, or the instruments available.

The most serious consequence is de-platforming — termination of the brokerage agreement or refusal to provide liquidity. In an environment where the reputation of a trading flow becomes an asset, its loss significantly complicates the search for new counterparties: brokers increasingly exchange client information through industry databases and informal channels.

4. Masking Arbitrage Order Flow: Techniques and Principles

4.1 The Fundamental Paradox: Why Perfection Is Toxic

The central paradox of modern arbitrage is as follows: order flow optimized across all classical parameters — maximum win rate, minimal losses on losing trades, precise temporal alignment with price movements — is the most easily identifiable. A statistically perfect order stream does not occur naturally among retail or uninformed institutional participants. Consequently, its high-confidence detection points to arbitrage activity.

This means that the objective of masking is not concealment of profitability per se, but the reproduction of statistical characteristics typical of non-directional order flow. In other words, the arbitrageur must appear to be a participant trading for reasons unrelated to information advantage — while retaining that advantage intact.

4.2 Timing Randomization: The Infrastructure Layer of Masking

One of the most widely employed techniques involves deliberately introducing random delays into the order execution process. When temporal intervals between orders exhibit high regularity — characteristic of algorithmic systems operating in hard real-time — this alone constitutes a strong signal for a detector. The introduction of pseudo-random noise with parameters that imitate the latency distribution of a human trader or an institutional execution algorithm substantially reduces classification accuracy.

In practical application, the SharpTrader platform provides built-in timing randomization mechanisms across numerous arbitrage strategies. SharpTrader’s randomization functionality allows parametric specification of random delay ranges between order submissions, variation of entry intervals as a function of market conditions, and thereby destruction of the deterministic temporal patterns characteristic of pure arbitrage algorithms. This makes the platform a notable example of how masking tooling has transitioned from bespoke internal development to commercially available solutions.

Technically, randomization is implemented through random number generators with specified distributions — for instance, log-normal distributions characteristic of human reaction times — or through sampling from historical data on the behavior of the target imitation group. A critically important nuance: the noise must not be uniformly distributed, as uniform distribution is itself a statistical anomaly readily identified by modern detectors.

4.3 Behavioral Mimicry: The PhantomDrift Strategy

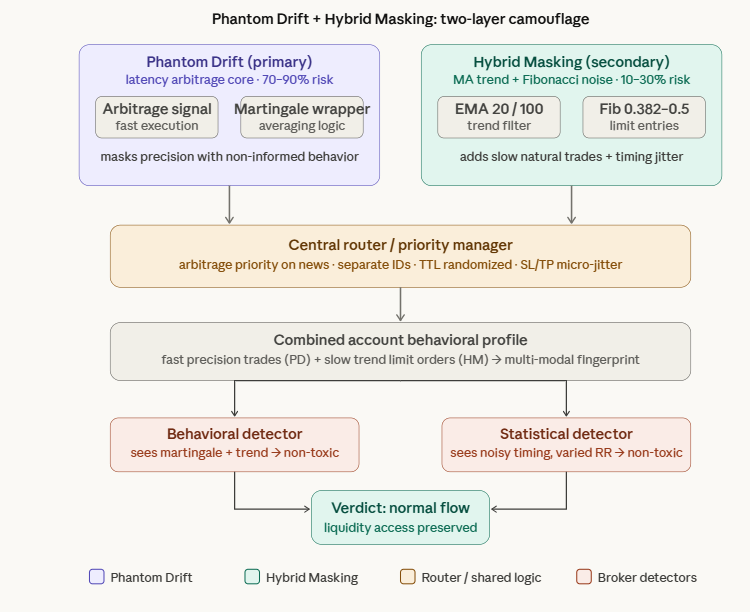

A deeper layer of masking involves not merely timing randomization, but imitation of behavioral patterns characteristic of specific classes of market participants. Among the most architecturally innovative approaches is the Phantom Drift strategy, developed by BJF Trading Group, which masks arbitrage activity by interweaving it with martingale-style trade management logic.

Phantom Drift — Core Concept: An arbitrage signal is executed within a behavioral wrapper that mimics martingale position management — systematic position doubling against adverse price movement. From the perspective of an external observer or broker detection system analyzing order series, such flow exhibits characteristics typical of an uninformed participant employing aggressive position management: increasing volumes against unfavorable moves, loss averaging, and an absence of obvious correlation with leading price signals. The arbitrage nature of the underlying signal is concealed by an apparently illogical risk-management pattern.

The effectiveness of this approach stems from the fact that martingale strategies are well known to brokers as a source of uninformed flow: their long-run unprofitability makes such clients desirable counterparties for market makers. Mimicry of this participant class creates robust cover for informed flow.

4.4 Hybrid Masking: Combining Layers of Protection

The logical next step in the behavioral mimicry technique is its combination with infrastructure randomization—an approach documented in BJF Trading Group’s published Hybrid Masking Strategy. This strategy uses an MA Trend + Fibonacci Pullback entry system as “positive-expectancy noise” running alongside the primary arbitrage module (Phantom Drift).

Hybrid Masking — Technical Architecture: The strategy identifies market trend direction using a dual-EMA system (EMA 20 as fast, EMA 100 as slow). Following a corrective MA crossover, Fibonacci retracement levels are calculated on the last directional impulse. Pending limit orders are placed at the 0.382–0.5 retracement zone with stops beyond the 0.786 level. This generates trade sequences — limit entries on trend pullbacks, variable holding periods, realistic SL/TP geometry — that are indistinguishable from systematic discretionary trading. Randomized TTLs (time-to-live) for pending orders, split entries between 0.382 and 0.5, and micro-jitter applied to SL/TP levels (±0.1–0.2×ATR) prevent the masking layer itself from forming a detectable pattern.

The fundamental value of the hybrid approach lies in its ability to attack two independent detection channels simultaneously. A behavioral detector analyzing trade decision logic sees a trend-following pattern. A statistical detector analyzing temporal flow characteristics sees an irregular, noisy order rhythm. To correctly classify such a flow as arbitrage, the detecting system must simultaneously overcome both defensive layers — a task substantially more complex than overcoming either individually.

4.5 Order Fragmentation and Multi-Account Diversification

An additional masking dimension involves distributing trading activity across multiple accounts and brokers such that no single counterparty obtains the complete picture required for identification. When a broker’s analytics sees only a fraction of the total order flow, the statistical significance of toxicity signals is reduced — particularly over short time windows.

Institutional execution algorithms — TWAP, VWAP, Implementation Shortfall — generate characteristic patterns of large order fragmentation. Imitating these patterns allows arbitrage flow to mimic institutional flow, which market makers perceive as less toxic. Diversification across instruments with differing correlation structures further diffuses the pattern characteristic of pure arbitrage.

5. AI versus AI: The Dynamics of Mutual Adaptation

5.1 Adversarial Dynamics and the Detection Race

The interaction between AI detectors on the broker side and masking systems on the arbitrageur’s side represents a canonical instance of adversarial dynamics — a phenomenon well studied in cybersecurity and described in adversarial machine learning theory. The detector trains on toxic flow patterns; the arbitrageur adapts their flow to evade detection; the detector retrains on new data — and so the cycle continues.

The fundamental distinction between this race and the traditional technological arms race is that the speed of adaptation is constrained not by physical parameters (network latency, processor speed) but by the rate of training data accumulation and computational resources for model retraining. This creates a qualitatively different dynamic: advantage is inherently temporary and inevitably erodes as the opposing side updates its models.

5.2 GAN-Like Architectures in Plausible Flow Generation

The most technologically advanced direction in this domain involves architectures analogous to Generative Adversarial Networks (GANs) for synthesizing order flow that is indistinguishable from non-directional trading. The concept: a generator model learns to produce order streams that a discriminator model (simulating the broker detector) cannot classify as toxic, with both components trained simultaneously in an adversarial process.

Practical deployment faces several constraints. Training the discriminator requires access to real data on how broker detectors respond to various patterns — information brokers are not inclined to share. Furthermore, the generated “plausible” flow must remain profitable, creating a tension between optimization for indistinguishability and optimization for returns.

5.3 Information Asymmetry and Its Implications

An important structural advantage for brokers in this race is access to aggregate data across the entire client base. The broker’s detector trains not only on a specific arbitrageur’s flow but on statistics across thousands of clients, enabling substantially more robust classifiers. The arbitrageur, conversely, observes only their own flow and market responses — materially limiting their ability to assess masking effectiveness.

The arbitrageur retains one key advantage, however: they know the true nature of their strategy and can deliberately engineer masking, while the detector operates on noisy aggregate data and must balance classifier sensitivity against specificity. A high false positive rate — erroneous classification of uninformed flow as toxic — is costly for the broker in terms of losing legitimate clients. This equilibrium tension limits how aggressively detectors can be calibrated, preserving operational space for well-designed masking systems.

6. Regulatory and Ethical Dimensions

6.1 The Boundary Between Masking and Manipulation

The regulatory status of order flow masking techniques remains legally undefined in most jurisdictions. The European MiFID II regulation contains market manipulation provisions, but these are formulated with respect to price manipulation rather than the obfuscation of trading behavior. The U.S. SEC Rule 15c3-5 (“Market Access Rule”) governs risk controls for market access but does not directly address the deliberate modification of order-flow statistical characteristics.

The conceptual line regulators draw runs between two types of conduct. The first type — legitimate execution optimization, i.e., any actions aimed at reducing market impact and improving execution quality — is standard institutional practice. The second type — actions that mislead other market participants or undermine pricing integrity — falls under prohibition. Masking from broker detection systems formally belongs to the first type, since it is directed at counterparty interaction rather than price manipulation. However, as regulatory thinking adapts to the realities of AI trading, this boundary may shift.

6.2 Tightening Requirements in the Context of Algorithmic Trading

Regulatory pressure on algorithmic trading broadly intensified over the 2023–2026 period. Requirements for algorithmic strategy registration, mandatory maintenance of trade decision logs, and their availability for regulatory review create operational burden and potentially open avenues for retrospective analysis of masking practices. In this context, documenting masking logic takes on a dual character: on one hand, it is a compliance requirement; on the other, it may constitute evidentiary material in investigations.

7. Conclusion

Arbitrage trading in 2026 constitutes a multi-layered competitive environment in which technological excellence is merely the starting point. Speed, feed quality, and hardware acceleration form a foundation without which participation is impossible — but they do not determine competitive outcomes. What determines outcomes is the participant’s ability to trade efficiently while remaining invisible to increasingly sophisticated order flow identification systems.

This shift has deep implications for industry structure. The barrier to entry in arbitrage has shifted from capital (infrastructure) to intellectual capital (the ability to develop and maintain effective masking techniques). The commercialization of masking tooling — clearly demonstrated by platforms such as SharpTrader with its built-in randomization mechanisms, and production-grade strategies such as Phantom Drift and the Hybrid Masking framework — signals that flow obfuscation is transitioning from bespoke expertise of the few to an industry standard.

Adversarial dynamics between detectors and masking systems will, in all likelihood, intensify as both sides expand their AI capabilities. In the long run, this may lead to one of two scenarios: either an equilibrium in which masking and detection costs neutralize arbitrage profits, rendering markets more efficient; or a permanent arms race in which only the most technologically advanced and adaptive participants survive. Which scenario materializes will be substantially determined by the regulatory environment, which, as of 2026, has not kept pace with the rate of technological change.

The social function of modern arbitrage also remains an open question: if classical arbitrage served as a mechanism for correcting price inefficiencies, enhancing pricing quality, then arbitrage forced to mask its activity may partially forfeit this function, substituting it with rent extraction under conditions of information asymmetry. For further reading on this evolving field, the BJF Trading Group blog maintains ongoing coverage of practical arbitrage strategy development, masking techniques, and platform updates.

Frequently Asked Questions (FAQ)

Q1: What is order flow toxicity, and why does it matter in 2026?

Order flow toxicity refers to the degree to which a client’s trading is systematically loss-making for the liquidity provider due to information asymmetry. In 2026, AI-powered broker analytics systems compute real-time toxicity scores and automatically widen spreads, apply last-look, or restrict access for identified arbitrageurs. A high toxicity score directly threatens the viability of the strategy.

Q2: Why has infrastructure advantage declined as a differentiator?

Colocation, direct data feeds, FPGA acceleration, and microwave links have become commercially available to all serious market participants. The capital barrier has fallen, producing infrastructure homogeneity among top-tier HFT firms. Competitive advantage has consequently migrated upstream to algorithm quality and, critically, the ability to avoid broker-side detection.

Q3: What is the Phantom Drift strategy, and how does it mask arbitrage?

Phantom Drift, developed by BJF Trading Group, is a latency arbitrage strategy that camouflages its activity by embedding arbitrage signal execution within a martingale-style behavioral wrapper. To broker surveillance systems, the resulting order stream resembles a non-informed participant employing aggressive position averaging — a behavioral profile associated with uninformed retail flow — while the underlying edge is derived from latency-based price discrepancies. Full documentation is available at: bjftradinggroup.com.

Q4: How does the Hybrid Masking Strategy differ from Phantom Drift?

While Phantom Drift addresses behavioral mimicry at the execution logic level, the Hybrid Masking Strategy operates as a secondary, auxiliary layer. It runs an independent MA Trend + Fibonacci Pullback strategy alongside the primary arbitrage module, generating a stream of realistic trend-following limit orders that normalize the account’s behavioral profile. The combination creates a multi-modal trading fingerprint that is substantially harder for both automated systems and human broker reviewers to classify as arbitrage.

Q5: Is order flow masking legal?

In most jurisdictions, flow masking techniques as currently practiced fall within the scope of legitimate execution optimization — standard institutional practice aimed at reducing market impact. They are directed at counterparty interaction, not price manipulation. However, the regulatory landscape is evolving: increasing requirements for algorithmic strategy documentation and audit trails mean that firms should maintain clear records of masking logic to demonstrate compliance intent.

Q6: What role does SharpTrader play in masking?

SharpTrader is BJF Trading Group’s flagship arbitrage and strategy platform. Beyond core arbitrage execution, it provides built-in parametric timing randomization across multiple strategy types, an AI Coder Assistant for developing custom filters, and native integration with the Phantom Drift and Hybrid Masking modules. It supports FIX API and cTrader connectivity, with full documentation at bjftradinggroup.com.

Q7: Will masking techniques remain effective as AI detectors improve?

The adversarial dynamic is self-perpetuating: as detectors improve, masking must adapt, and vice versa. The structural advantage of well-designed masking lies in its multi-channel approach — attacking behavioral and statistical detection dimensions simultaneously. Hybrid architectures combining diverse, loosely correlated behavioral patterns (as in the Hybrid Masking framework) are more durable than single-technique approaches precisely because overcoming them requires simultaneously defeating multiple independent detection systems.

References and Further Reading

Academic Sources

- Glosten, L.R., & Harris, L.E. (1988). Estimating the components of the bid/ask spread. Journal of Financial Economics, 21(1), 123–142.

- Easley, D., Lopez de Prado, M.M., & O’Hara, M. (2011). The microstructure of the ‘Flash Crash’: Flow toxicity, liquidity crashes, and the probability of informed trading. Journal of Portfolio Management, 37(2), 118–128.

- Budish, E., Cramton, P., & Shim, J. (2015). The High-Frequency Trading Arms Race: Frequent Batch Auctions as a Market Design Response. Quarterly Journal of Economics, 130(4), 1547–1621.

- Goodfellow, I., Pouget-Abadie, J., Mirza, M., et al. (2014). Generative Adversarial Networks. Advances in Neural Information Processing Systems, 27.

- Hasbrouck, J. (2007). Empirical Market Microstructure. Oxford University Press.

- Aldridge, I. (2013). High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems (2nd ed.). Wiley.

- Lopez de Prado, M. (2018). Advances in Financial Machine Learning. Wiley.

- European Securities and Markets Authority (ESMA). (2021). MiFID II/MiFIR Review Report on Algorithmic Trading.

BJF Trading Group Documentation and Blog

- BJF Trading Group Inc. (2025). Hybrid Masking Strategy: MA Trend + Fibonacci Pullback Entry as ‘Noise’ for Arbitrage alongside Phantom Drift. bjftradinggroup.com

- BJF Trading Group Inc. (2025). How to Mask Latency Arbitrage in Forex Trading — Complete Guide Part 2 (Phantom Drift). bjftradinggroup.com

- BJF Trading Group Inc. SharpTrader Platform Documentation. bjftradinggroup.com

- BJF Trading Group Inc. Blog — Arbitrage Software, Forex Trading, Strategy Development. bjftradinggroup.com/blog

- BJF Trading Group Inc. (2026). Does Retail Have a Chance in Arbitrage? bjftradinggroup.com

- BJF Trading Group Inc. (2026). White Paper 2026: The Future of Economic News Trading. bjftradinggroup.com

© 2026 BJF Trading Group Inc. | Ontario, Canada | bjftradinggroup.com

This article is provided for informational and educational purposes only and does not constitute financial advice.