Deutsch

Deutsch 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

White Paper 2026: The Future of Economic News Trading — A New Wave of Volatility, Algorithms, and AI Infrastructure Monday December 8th, 2025 – Posted in: News Trading Software

Introduction

Economic news trading has traditionally attracted traders with its high volatility, fast price movements, and the potential to earn profits within seconds. However, in recent years the market has undergone a technological leap that has radically transformed the entire structure of order execution, broker behavior, and the reaction speed of major participants.

In 2024–2025, banks, prop-trading firms, and systematic hedge funds deployed fully automated frameworks for processing economic releases, built on machine learning, predictive statistics, and ultra-low-latency communication channels. In 2026, these trends intensify, creating a new environment in which the classical approach to news trading becomes less effective—but new methods emerge, accessible to both automated and professional traders.

The purpose of this document is to provide a deep overview of the 2026 news-trading landscape:

- how liquidity sources have changed,

- what is happening with spreads and slippage,

- which algorithms dominate the market,

- which strategies remain profitable,

- the role of masking technologies and AI-driven order depersonalization,

- how traders can adapt to the new environment.

The News Trading Market in 2026: Infrastructure Transformation

1.1. New Rules from Banks and Liquidity Providers

News trading is no longer a simple “speed competition” among retail traders. Winners are now those who have access to:

- machine-readable news feeds,

- direct data-source connectivity,

- release-analysis algorithms operating under 10 ms,

- low-latency matching engines,

- liquidity streams optimized for volatility spikes.

Banks and funds rely on predictive models that analyze not just the economic indicator itself but the probability of market reaction. This radically changes price behavior during the first milliseconds after the release.

Retail traders cannot compete on speed under these conditions, but they can trade secondary impulses and algorithmic patterns.

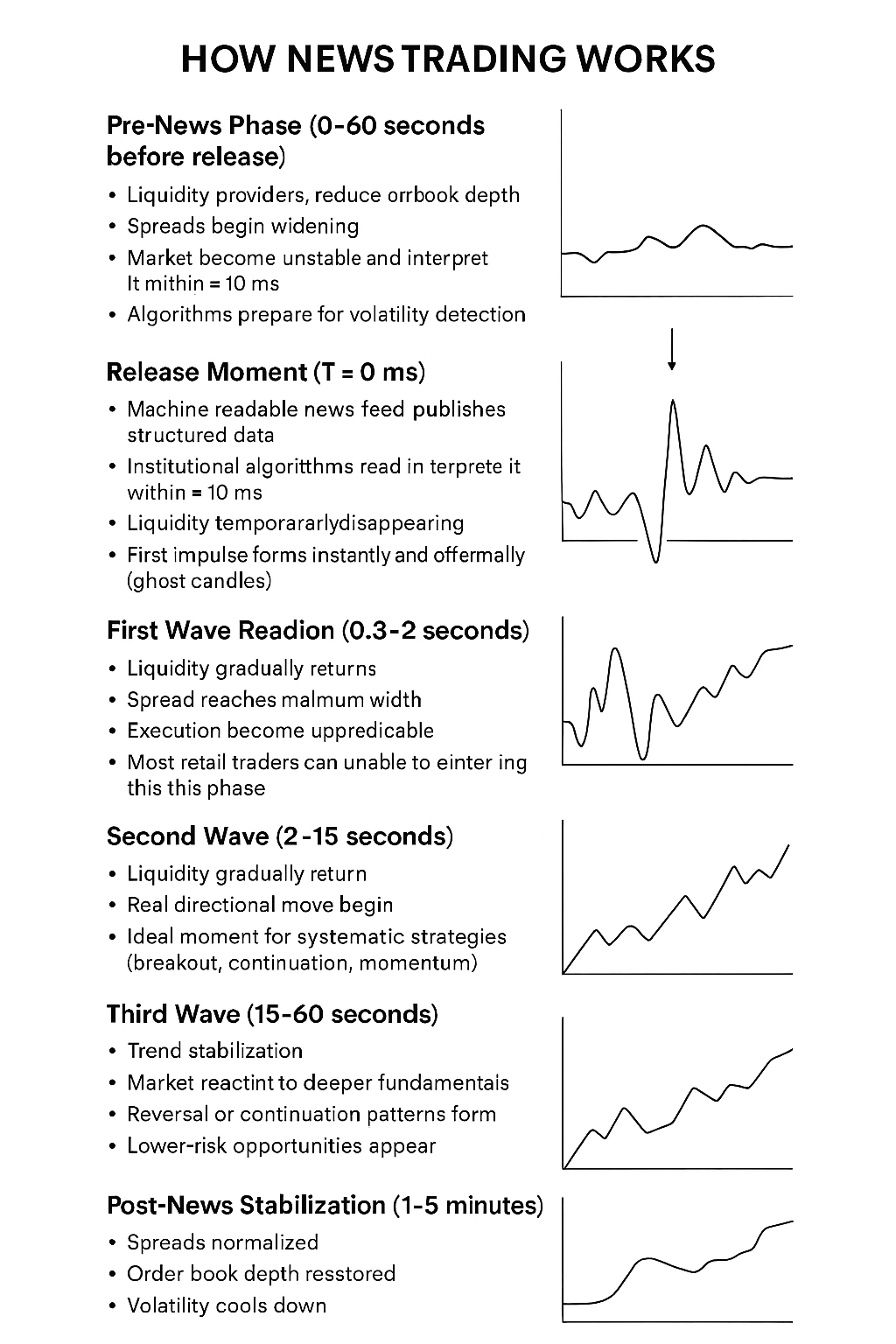

Increased Volatility and Reduced Liquidity During Releases

2.1. The Liquidity Paradox

For many years, it was believed that liquidity increases during major macroeconomic releases.

Since 2023, the opposite started happening:

Liquidity collapses in the first 50–150 ms as LP algorithms reassess risk and reconfigure quotes.

As a result:

- spreads widen,

- slippage increases,

- orders are filled partially or not at all,

- “empty candles” become normal.

2.2. Consequences for Traders

- STOP orders receive severe slippage, often several times higher than expected.

- LIMIT orders may not fill at all due to vanishing liquidity.

- Impulses become shorter but stronger, creating false breakouts.

- The post-initial retracement has become the primary entry point.

How Brokers Adapt to News Trading in 2026

3.1. Spread Widening as an Industry Standard

While in 2020–2022 large spread expansions were rare, by 2026:

- many brokers widen spreads 3–10 seconds before a release,

- LP risk algorithms generate “defensive” pricing,

- ECN networks automatically reduce depth of book.

This makes classical Buy Stop / Sell Stop strategies extremely risky.

3.2. Tougher Execution Rules

Brokers now implement:

- restrictions on news-moment trading,

- minimum distance requirements for stop orders,

- toxicity-pattern scanning (TCA + AI),

- analysis of order-submission speed.

The goal is to protect themselves from instant arbitrage strategies.

The AI Revolution: How Artificial Intelligence Reshapes News Trading

4.1. Predicting Market Reaction with Machine Learning

In 2026, AI systems analyze:

- historical reaction patterns,

- pre-release volatility,

- cross-asset correlations,

- probability of false breakouts,

- liquidity parameters,

- order book velocity.

This enables probabilistic prediction of behavior, rather than trying to guess the economic number itself.

4.2. AI-Based News Filtering

Modern systems can:

- ignore releases unlikely to generate movement,

- select optimal strategies for different news types,

- dynamically set Stop Loss and Take Profit distances,

- determine optimal post-release entry timing.

This increases signal quality and reduces risk.

Effective News Trading Strategies in 2026

Below are strategies that remain profitable despite higher competition and stricter execution conditions.

5.1. Post-News Volatility Strategy (Entry After 2–15 Seconds)

The strategy is based on:

- the first milliseconds being dominated by HFT,

- real direction forming later,

- liquidity returning after 1–3 seconds.

Effective on major high-impact releases such as:

- NFP

- CPI

- PMI

- FOMC

- ECB Rate Decision

5.2. Fade-the-News: Counter-Trading After Hyper-Impulses

Mechanism:

- The release triggers a strong price spike.

- LP and HFT algorithms unwind positions.

- Price returns toward mean levels.

Especially effective on:

- GBPUSD

- AUDUSD

- JPY crosses

- CAD during oil-related releases

5.3. Secondary and Tertiary Impulse Trading

Most news moves occur not in one candle, but in waves:

- The first — chaotic, noisy, misleading.

- The second — forms the true directional bias.

- The third — confirms the trend.

Trading on the second or third wave is safer and more consistent than entering on the first.

5.4. OCO Strategies (One Cancels the Other)

Many trading platforms require OCO logic to be implemented via robots.

Modern versions include:

- intelligent entry delay,

- duplicate-order protection,

- slippage management,

- toxicity control and masking.

5.5. Correlation-Driven News Pair Trading

Trading correlated asset pairs such as:

- EURUSD vs USDCHF

- EURJPY vs USDJPY

- GBPUSD vs EURGBP

Allows capturing arbitrage-like opportunities created by post-news imbalances.

Masking and AI-Evasion: A Critical Success Factor in 2026

In 2026, brokers widely use:

- order-frequency and structure analysis,

- latency arbitrage behavior detection,

- correlation of order timing with news calendars,

- strategy-classification models.

Thus masking becomes mandatory.

Modern masking methods include:

- randomizing order-submission time (± X ms),

- varying order sizes,

- using multiple entry logics,

- distributing trades across multiple accounts,

- simulating “human-like” order patterns.

Systems without masking quickly become unprofitable due to degraded execution.

NewsAutoTraderPro: Next-Generation News Automation with Machine-Readable Data Access

Modern news trading requires not only fast reaction but access to professional data streams that deliver information earlier than standard economic calendars.

NewsAutoTraderPro is an advanced next-generation system utilizing machine-readable news feeds and instant-reaction algorithms. Unlike classical EAs that rely on delayed calendars or static input times, NewsAutoTraderPro connects to fast MLR (Machine-Readable Releases) streams, allowing it to detect the exact moment of a release and make a trading decision almost instantly.

Its decision logic is multi-layered:

- receives structured data (time, value, forecast, deviation, importance),

- compares actual vs expected values,

- determines primary directional bias,

- decides whether to enter immediately, delay execution, or skip the trade due to low volatility or high risk.

This allows NewsAutoTraderPro to enter positions faster than typical automated systems relying on timers or local calendars.

Unique Pre-News Locking Feature

One of the system’s key advantages is the ability to pre-open a hedged (locked) structure before the news.

Algorithm:

- Before the release, the robot opens a Buy+Sell lock, distributing risk across two opposite positions.

- After the release, it analyzes the actual value, market reaction, and impulse strength.

- The unnecessary side of the lock is closed, and the remaining side becomes a directional position.

- If needed, position size is increased or managed via adaptive trailing.

This approach avoids most negative effects of the first volatility wave—slippage, missing liquidity, wide spreads—while extracting value from the subsequent impulse.

Intelligent Filtering and Risk Management

NewsAutoTraderPro supports:

- filtering by news type,

- separate rules for high-, medium-, and low-impact events,

- configurable entry delays,

- slippage-limit controls,

- risk limits in low-liquidity conditions.

According to the official product page (https://bjftradinggroup.com/product/newsautotraderpro/), the robot includes multiple professional modes suitable for both classical news trading and aggressive, fast-data strategies with adaptive order management.

NewsAutoTraderPro as Part of the 2026 Professional News-Trading Ecosystem

As the market shifts toward automation, fast data processing, and increased broker surveillance, NewsAutoTraderPro becomes a key tool for traders operating during economic releases. With access to fast machine-readable feeds, adaptive algorithms, and pre-news hedging, the system provides advantages previously available only to technological prop-trading firms.

Execution Infrastructure: Technical Requirements for 2026

7.1. VPS with 1–2 ms Latency to Broker

Even non-HFT strategies suffer when latency exceeds 5–10 ms during news.

7.2. Accelerated Algorithms Inside Expert Advisors

Modern news robots must:

- minimize loop operations,

- use pre-computations,

- avoid heavy operations during releases,

- rely on low-level functions.

7.3. Slippage Control

Modern systems actively manage:

- maximum allowed slippage,

- order-size limits,

- number of retry attempts.

Most Profitable News Releases in 2026

United States

- NFP

- CPI

- Core PCE

- FOMC Rate Decision

- ISM PMI

Europe

- ECB Press Conference

- CPI Flash Estimate

- German ZEW & IFO

United Kingdom

- BOE Rate Decision

- CPI

- GDP

Canada

- CAD CPI

- BoC Rate Decision

- Employment Change

Japan

- BOJ Press Conference

- Interventions (always high-risk)

These releases generate reliable impulses suitable for algorithmic trading.

Risks Associated With News Trading

9.1. Slippage

The primary issue in 2026.

Only adaptive systems that account for liquidity dynamics can maintain performance.

9.2. Signal Uncertainty

The market is increasingly unpredictable due to algorithmic concentration.

9.3. Broker Restrictions

Toxicity filters can severely worsen execution.

9.4. Non-Trending Volatility

Strong impulses may rapidly reverse, forming “saw-tooth” patterns.

Future Outlook: Where News Strategies Are Heading

10.1. Growth of AI-Driven Trading Systems

By 2027, most successful strategies will rely on:

- machine-based liquidity analysis,

- volatility forecasting,

- dynamic adaptation to market conditions.

10.2. Liquidity Decentralization

Crypto-dollars, tokenized assets, and alternative dealing pools will reshape execution models.

10.3. Rising Demand for Hybrid Strategies

News trading will blend more often with:

- arbitrage,

- scalping,

- correlation models,

- long-term fundamental analysis.

Conclusion

Economic news trading in 2026 is undergoing a fundamental transformation. Old methods based on placing pending orders before releases are losing effectiveness due to:

- aggressive AI-driven bank infrastructure,

- declining liquidity,

- widening spreads,

- increased slippage,

- toxicity-traffic filters.

However, the market remains rich with opportunity for those who adapt.

Critical success elements include:

- AI-powered predictive models,

- trading secondary and tertiary impulses,

- robust masking technology,

- advanced execution infrastructure,

- dynamic risk management.

For traders and system developers, 2026 marks the era where winners are no longer the fastest—but the most adaptive.

FAQ — News Trading in 2026 & NewsAutoTraderPro

1. What makes news trading in 2026 different from previous years?

In 2026, the market is shaped by ultra-fast machine-readable news feeds, AI-driven liquidity engines, dynamic spreads, and aggressive risk controls from liquidity providers. Price reactions are shorter, sharper, and less accessible to manual traders. Success now depends on adaptive strategies, intelligent automation, and access to fast and structured data — not raw execution speed alone.

2. Why do spreads widen so aggressively before and after economic releases?

Liquidity providers reduce their exposure during high-risk periods. Their AI-based systems automatically enlarge spreads, pull pending liquidity from the book, or provide only shallow quotes. This protects LPs from unpredictable volatility but increases execution costs for traders. Widening spreads have become a normal part of modern news trading.

3. Why does slippage occur even with high-quality brokers?

Slippage is caused by rapid price movement and fragmented liquidity immediately after a release. When the market moves faster than orders can be matched, execution happens at the next available price. Even institutional traders experience slippage — it is a fundamental characteristic of news-driven markets.

4. Can manual traders still profit from news events in 2026?

Manual trading on the first impulse is nearly impossible due to the dominance of automated systems. However, traders can still profit from:

- second and third price waves,

- post-news volatility patterns,

- reversal spikes,

- correlation imbalances between currency pairs.

These strategies do not require millisecond execution.

5. What is NewsAutoTraderPro and how is it different from other news trading tools?

NewsAutoTraderPro is an advanced automated system that uses machine-readable news feeds and real-time analysis to make instant trading decisions. Unlike traditional news robots that rely on delayed calendars or manual input, it reacts the moment structured data is released and can adjust its strategy dynamically based on volatility and deviation levels.

6. How does the lock (hedging) mechanism work before a news release?

The system can open a protective lock (buy + sell) shortly before the release. After the actual news value arrives:

- NewsAutoTraderPro analyzes the deviation and market reaction,

- closes the losing side of the lock,

- keeps the profitable direction open,

- and continues managing the trade adaptively.

This approach minimizes execution risks such as spread widening and slippage while allowing the system to capture the main post-news move.

7. Does NewsAutoTraderPro require ultra-low latency to be effective?

No. While low latency improves overall performance, the system does not rely on beating institutional HFTs. The core advantage is direct access to structured news data and intelligent logic — not raw speed. Its lock mechanism and adaptive post-news strategies also reduce dependency on microsecond execution.

8. How does the system filter which news events to trade?

NewsAutoTraderPro includes a built-in classification engine that evaluates:

- the importance of the event,

- expected volatility,

- historical market reaction,

- correlation with other instruments,

- deviation significance (actual vs. forecast).

It trades only when the statistical probability of meaningful movement is high.

9. Is news trading risky?

Yes. All news trading involves elevated risk due to fast price movement, temporary liquidity gaps, and unpredictable reactions. Traders must use proper risk management, understand volatility behavior, and accept that slippage cannot be fully eliminated — only managed.

10. Can NewsAutoTraderPro be used with any broker?

The system can technically run with most brokers, but performance depends on the broker’s execution model, liquidity quality, filled-order tolerance, and treatment of high-volatility trading. Brokers with dynamic spreads and aggressive risk controls may reduce efficiency. Choosing the right trading environment is critical.

11. Does the system rely on martingale, grid, or dangerous money management?

No. NewsAutoTraderPro does not use martingale, grid averaging, or any form of exponential risk increase. All position sizing is controlled, transparent, and based on predefined risk parameters.

12. Is backtesting useful for news trading systems?

Standard backtesting is unreliable for news trading because historical tick data does not accurately reproduce:

- latency,

- depth-of-market fluctuations,

- slippage,

- spread explosions,

- liquidity gaps.

Only forward testing and live execution reflect real behavior. This applies to all news strategies, not only automated ones.

13. How does NewsAutoTraderPro avoid AI-based broker detection?

Modern brokers classify trading strategies using AI-driven toxic-order-flow analysis. NewsAutoTraderPro includes:

- randomized execution delays,

- dynamic order sizing,

- multiple entry logics,

- non-predictable timing patterns,

- variable behavior across accounts.

This reduces detectability and makes order flow appear more natural and less algorithmic.