Deutsch

Deutsch 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

Phantom Drift – Bypassing Broker Anti-Arbitrage Plugins Friday August 22nd, 2025 – Posted in: Arbitrage Software – Tags: allowed arbitrage, arbitrage bot, forex arbitrage, Latency Arbitrage, phantom drift

Phantom Drift is a hybrid trading solution that combines the advantages of arbitrage with the resilience of martingale-style risk management. Its goal is to ensure steady capital growth while minimizing the risk of broker detection.

Video 1. – Short YouTube video about Phantom Drift performances.

The strategy demonstrates a smooth equity curve and maintains the execution speed of an arbitrage system.

| Phantom Drift Metric | Value |

| Total Trades | 4821 |

| Winning Trades | 2785 |

| Losing Trades | 1955 |

| Win Rate % | 57.77 |

| Total Profit | 62359.36 |

| Average Profit per Trade | 13.0 |

| Max Single Profit | 9800.0 |

| Max Single Loss | -3215.4 |

| Most Profitable Symbol | XAUUSD |

Advanced Phantom Drift Metrics

| Advanced Metric | Value |

| Average Trade Duration (sec) | 9492.03 |

| Median Trade Duration (sec) | 60.0 |

| Arbitrage-like Trades (<60s) | 2101 |

| Arbitrage Trade % | 43.58% |

Phantom Drift Equity Curve

(click to view all performance metrics)

How Phantom Drift Masks Arbitrage

Typical arbitrage can be detected by brokers due to ultra-short holding times and repetitive patterns. Phantom Drift solves this problem by:

- Stepwise position building (emulating martingale).

- Extended holding time compared to pure arbitrage (average > 2 hours).

- Flexible lot sizing instead of linear doubling.

- Mixing instruments, with a strong focus on gold (XAUUSD).

- Arbitrage-like trades make up less than 50% of the overall activity, hidden in the broader stream of longer-term trades.

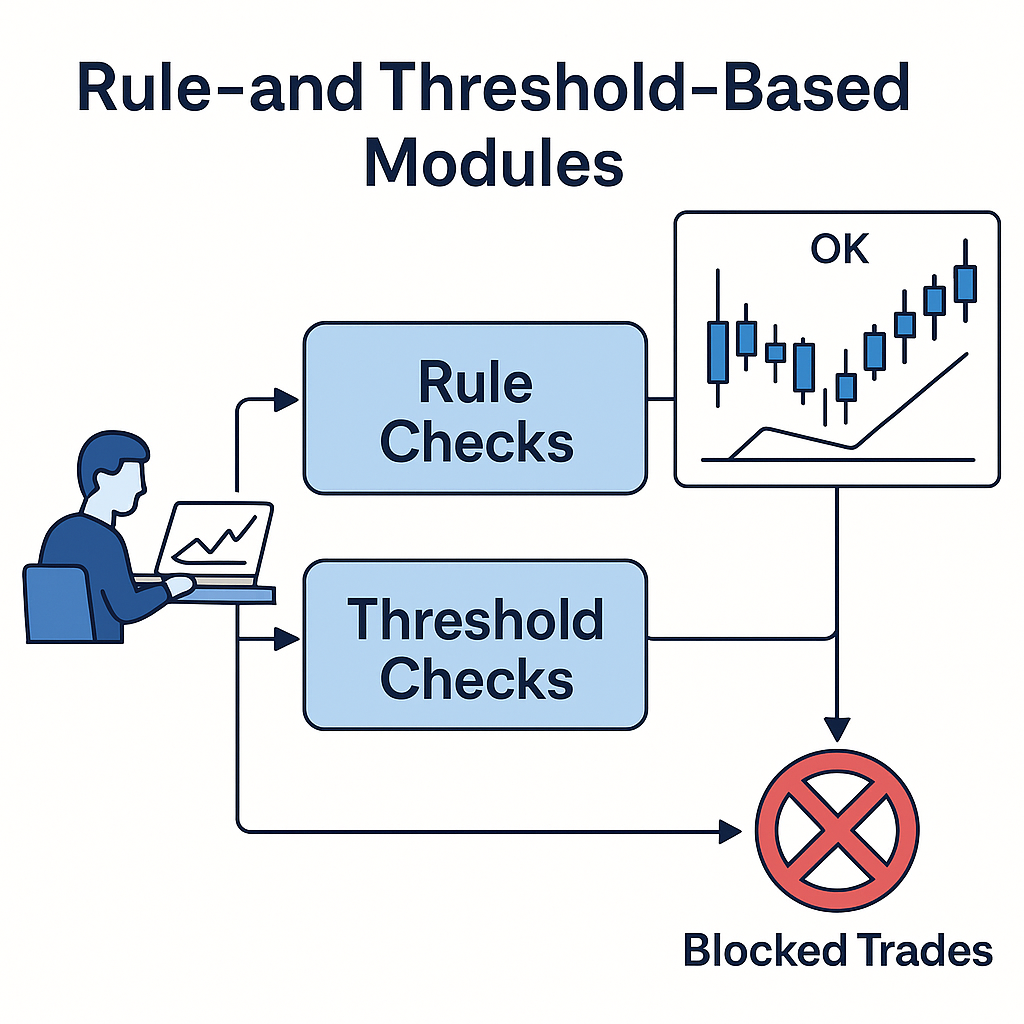

Bypassing Broker Anti-Arbitrage Plugins

Broker anti-arbitrage solutions can be divided into two classes. The first is rule- and threshold-based modules implemented by standard retail brokers: they block closures or re-entries within a minimum holding period and limit order frequency, thereby cutting short scalping bursts and news-driven spikes.

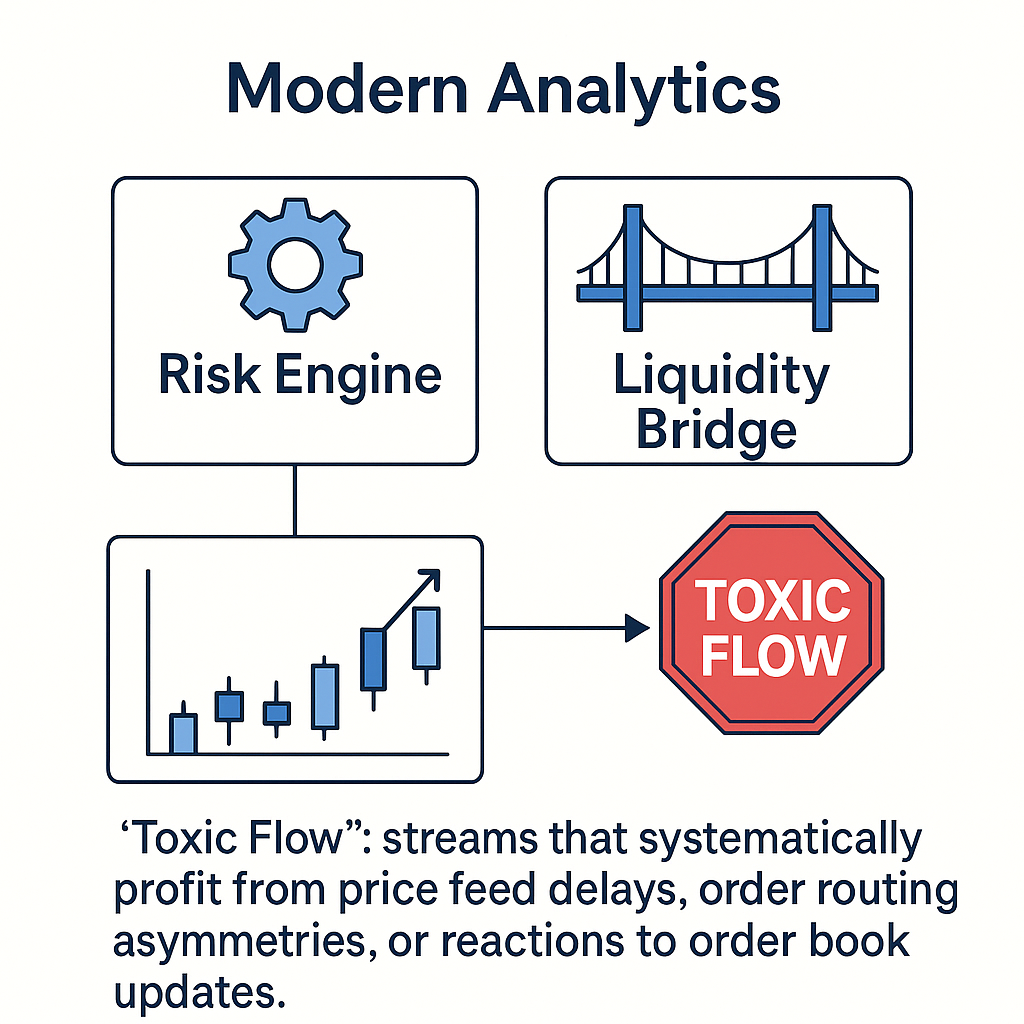

The second is more modern analytics where risk engines and liquidity bridges tag ‘toxic flow’: streams that systematically profit from price feed delays, order routing asymmetries, or reactions to order book updates. Here, the metrics include distributions of holding time, speed of reaction to quotes, clustering of entries around news, and profit-after-execution curves. If trades systematically resolve profitably within tiny horizons, they are flagged as toxic. Liquidity hubs and technology providers further expand this with AI-driven simulators and replay engines that profile latency, toxicity, and anomalous patterns in real-time. Recent research even documents neural network methods that update online to predict trade toxicity in milliseconds (PULSE, for example, outperformed logistic regression and random forests in classifying toxic trades for brokers). Finally, so-called ‘virtual dealer’ layers add deliberate delays or re-checks and apply different execution modes during news or gaps to neutralize fast arbitrage bursts.

Phantom Drift is designed to weaken its projection across all these detection axes. The heavy tail of trade duration and nonlinear lot progression break the simple anti-scalper rules (average holding time is high, with no dominant short mode). The flow of entries is dispersed across time and instruments, so clustering around news or tick updates is statistically weak. Abandoning strict doubling and varying exit logic smooths the ‘win-only’ signature on which toxicity detectors train. Its slippage distribution and holding-time profile appear human-like, with multiple modes and long tails, reducing the chance of being flagged by liquidity analytics. By limiting exposure during high-impact announcements and moderating order modification speed, its footprint remains within normal corridors of risk monitoring. This is not ‘hacking’ the plugins but designing a behavioral profile that statistically converges with healthy client flow—the kind which AI-based toxicity monitors and liquidity providers consistently classify as low risk.

Conclusion

Phantom Drift combines the best of both worlds: arbitrage opportunities and martingale resilience. This makes it a powerful and safe product for traders and prop firms, ensuring steady capital growth, broker-friendly execution, and transparent performance statistics.

❓ FAQ – Phantom Drift Strategy

1. What is Phantom Drift?

Phantom Drift is a hybrid trading strategy that combines arbitrage precision with martingale-style risk management. Its design ensures consistent growth while disguising arbitrage patterns from broker detection systems.

2. How is it different from classic arbitrage?

Unlike pure arbitrage, which relies on ultra-short trades and often wins 100% of the time, Phantom Drift:

-

Uses longer average holding times (~2h 38m).

-

Maintains a balanced win/loss ratio (~58% win rate).

-

Includes controlled drawdowns to mimic natural trading activity.

This makes the strategy more sustainable and broker-friendly.

3. Why does Phantom Drift not win 100% of trades?

Winning 100% of trades is a red flag for brokers and risk engines. Phantom Drift intentionally balances profitable and losing trades, which makes it look like a normal, discretionary trading strategy while still delivering strong profitability.

4. How does Phantom Drift bypass broker anti-arbitrage plugins?

It avoids detection by:

-

Dispersing trades across time and instruments.

-

Using nonlinear lot progression instead of rigid doubling.

-

Generating “human-like” distributions of slippage and holding time.

-

Limiting exposure during high-impact news events.

These techniques disguise arbitrage as natural trading flow.

5. What instruments does Phantom Drift trade?

The main focus is XAUUSD (Gold) due to its liquidity and volatility. However, it also trades major FX pairs like EURUSD, GBPUSD, and USDJPY for diversification.

6. What were the account results shown in the report?

-

Start Balance: $9,800 (June 11, 2025)

-

Current Balance: $62,000+

-

Total Trades: 4,821

-

Win Rate: 57.7%

-

Max Profit per Trade: $9,800

-

Max Loss per Trade: –$3,215

7. Is Phantom Drift suitable for prop firms?

Yes. Its balanced risk profile, disguised flow, and consistent equity curve make it well-suited for prop firm challenges and long-term funded trading.

8. Can brokers still detect it?

In the majority of cases, no. Phantom Drift’s behavioral profile blends into healthy client flow and is classified as low-risk by most monitoring systems.

However, in some cases, a dealing desk may perform manual analysis and decide to increase execution times if they see the strategy is consistently profitable.

9. Can you describe the strategy’s algorithm?

The exact algorithm is not disclosed. This ensures brokers cannot adapt their plugins to counter the approach. What matters is the outcome: steady growth, realistic trade distribution, and sustainable performance.

10. Is taker arbitrage realistically achievable on major liquidity providers under a no-last-look setup with IOC/FOK orders and short TTLs?

A:

Yes, taker arbitrage is achievable under these conditions, but with important caveats:

-

Liquidity Providers: True no-last-look streams from LPs (such as Equiti, MAS, or others) allow immediate or rejected fills without last-look filtering. However, some LPs still apply hidden throttling or soft checks during aggressive flows.

-

IOC/FOK and TTL: Using Immediate-or-Cancel (IOC) or Fill-or-Kill (FOK) orders combined with short time-to-live (TTL) parameters prevents stale fills and reduces adverse selection. The challenge is balancing TTL short enough to avoid latency issues, but long enough to be executable across venues.

-

Practical Challenges:

• Ultra-low-latency infrastructure (colocation in NY4, LD4, TY3, etc.) is crucial.

• LPs monitor “toxic flow,” so systematic arbitrage may result in widened spreads, throttled fills, or degraded stream quality.

• Smaller order sizes and distributing flow across multiple LPs improves sustainability.

👉 In summary: It is realistically achievable if supported by the right infrastructure and execution logic. Proper flow management and diversification are essential to keep the strategy sustainable.