Deutsch

Deutsch 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

Hybrid Masking Strategy: MA Trend + Fibonacci Pullback Entry as “Noise” for Arbitrage (alongside Phantom Drift) Wednesday October 22nd, 2025 – Posted in: Arbitrage Software, Forex trading

roadmap for an auxiliary strategy designed to mask latency arbitrage. In the initial phase, some modules and ideas will not be implemented. A simplified version will be released first and will make it according to the plan described here, as well as based on your feedback and suggestions. Key idea: this is not a primary profit-generating strategy; it is a tool for plausible masking of arbitrage activity. Its job is to produce a sequence of broker-credible “market” actions (trend- and pullback-based), smooth the account’s behavioral profile, reduce correlation with arbitrage signals, and thereby lower the probability that anti-arbitrage plugins will trigger. Core PnL expectations come from arbitrage (e.g., Phantom Drift); this strategy serves as “decor” and “positive-expectancy noise.”

Why latency arbitrage masking is needed and why MA+Fibo

Arbitrage strategies—especially latency/mispricing variants—leave a recognizable behavioral footprint: extremely short holding times, repetitive entry patterns, similar reactions to news/micro-liquidity dislocations. Modern anti-arbitrage tools analyze:

- the density and synchronicity of entries relative to news events;

- ultra-tight stops/takes and frequent partial closes;

- identical symbols/timeframes/time-of-day activity;

- the relationship between execution speed and profit profile.

A masking layer must:

- make human-trader sense (so behavior looks like “discretionary systematic trading”),

- fit in timing and symbols around arbitrage activity (without tight synchronization),

- maintain modestly positive expectancy with sound risk management, and

- keep a conservative trade frequency (to avoid ballooning fees or “shouting” with activity).

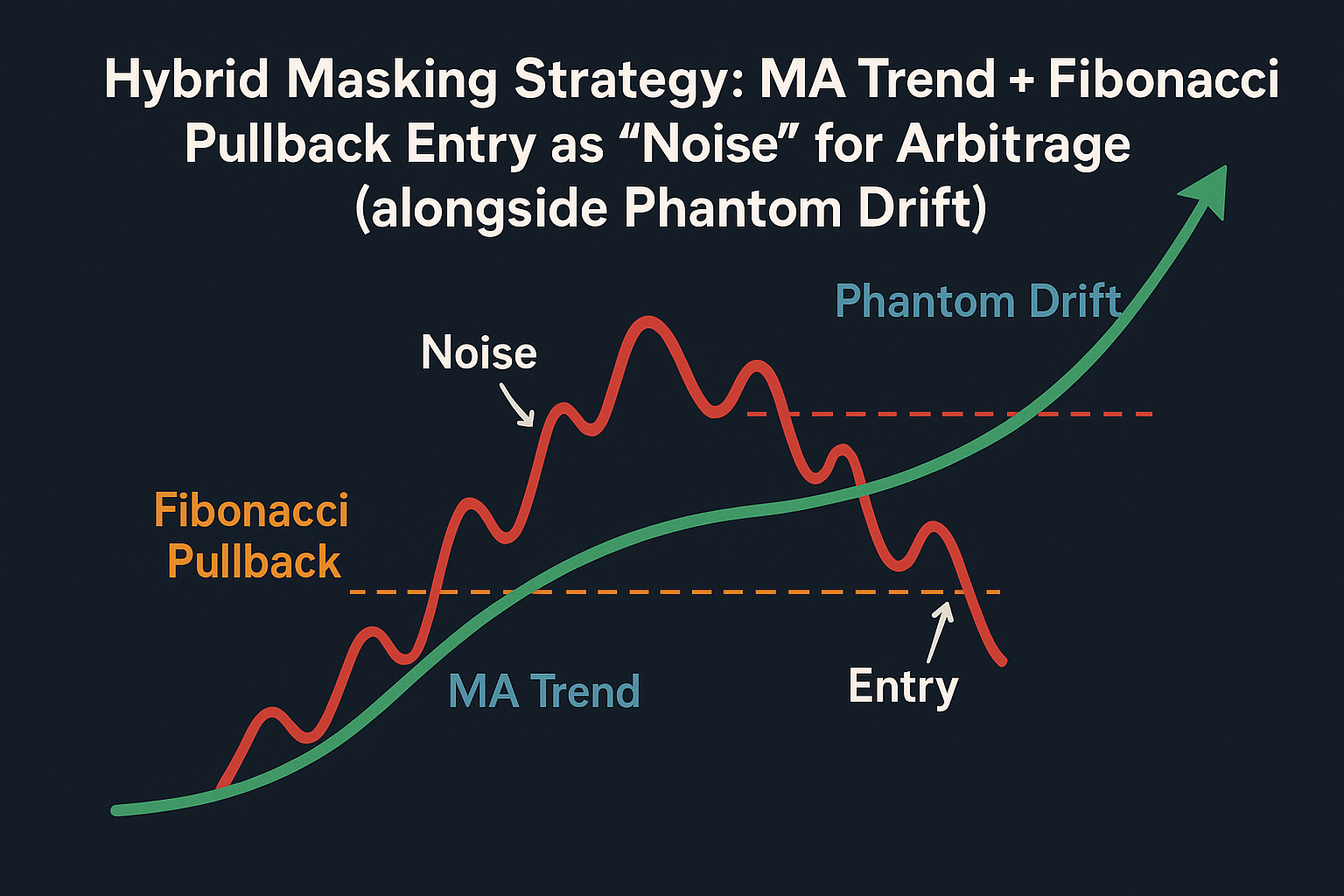

The MA-trend + Fibonacci pullback entry hybrid meets these requirements:

- it looks like a classic trend-following with pullback entries approach;

- it’s understandable to brokers and risk desks: trend confirmed by MAs; entry anchored to 0.382–0.5, stop beyond 0.786/local extreme;

- it’s easy to code and maintain; the logic is portable across standard trading platforms (e.g., cTrader, FIX-API terminals, NinjaTrader, etc.).

Pic 1. – Hybrid Latency Arbitrage Masking Strategy

Pic 1. – Hybrid Latency Arbitrage Masking Strategy

Latency Arbitrage masking strategy Core logic (formalization)

2.1 Determining the “background” trend

- MA_slow: EMA(100) — primary trend.

- MA_fast: EMA(20) — local oscillations.

Rule:

- If MA_fast > MA_slow → treat as uptrend.

- If MA_fast < MA_slow → treat as downtrend.

2.2 Identifying the start of a pullback We treat a cross of MA_fast and MA_slow against the trend as the pullback trigger:

- In an uptrend, wait for MA_fast to cross below MA_slow → confirm correction has started.

- In a downtrend, wait for MA_fast to cross above MA_slow → confirm corrective pullback.

Important: we do not enter on the cross itself—it is only the trigger to draw Fibonacci and prepare a pending order. 2.3 Building Fibonacci on the last impulse After confirming a pullback, identify the last impulse in the trend direction:

- Uptrend: from the local low to the local high of the impulse.

- Downtrend: from the local high to the local low.

Apply 0.236, 0.382, 0.5, 0.618, 0.786. In practice, 0.382–0.5 are the sweet spot for entries—between “buying cheap” and “not waiting for an overly deep retrace.” 2.4 Placing pending orders

- Uptrend: place Buy Limit at 0.382 or 0.5 (optionally split into two tickets).

- Downtrend: place Sell Limit at 0.382 or 0.5.

Stop Loss: beyond 0.786 (or beyond the local extreme—more conservative). Take Profit: conservative—back to 0.0 (retest of the impulse top/bottom), or aggressive—towards the 1.618 extension. 2.5 Additional filters (as needed; can be implemented by the trader via an AI Coder assistant)

- ADX > 20: trade only in trending phases.

- ATR bar filter: ignore if the trigger bar is too large (> 2×ATR) to avoid panic-chasing.

- Session filter: e.g., exclude the Asian session on majors if historically noisier.

Video 1. – How to code filter with SharpTrader AI Coding assistant

Default parameters and meaning

| Parameter | Value | Comment |

| MA_fast_period | 20 | EMA sensitive to local impulse |

| MA_slow_period | 100 | EMA smoothing the background |

| Fibo_entry | 0.382 (or 0.5) | optional split: 50% at 0.382, 50% at 0.5 |

| StopLoss_Fibo | 0.786 | or slightly beyond the local extreme |

| TakeProfit_Fibo | 0.0 or 1.618 | depends on masking goal and trade duration |

| Timeframe | H1/H4 | less noise, more “human-like” holding patterns |

| Filter_ADX | 20 | avoid chop |

Timeframe note: on H1/H4 trades last longer; the “limit + trend” combo looks like a swing idea, behaviorally far from a typical arbitrage profile.

Pseudocode

if MA_fast > MA_slow: # Uptrend if CrossDown(MA_fast, MA_slow): # retracement started swing_low, swing_high = find_last_swing_up() fib = calc_fibo(swing_low, swing_high) # {0.382: …, 0.5: …, 0.786: …, 0: …} place_pending_buy(price=fib[0.382], sl=fib[0.786], tp=fib[0]) # optional second order at 0.5 elif MA_fast < MA_slow: # Downtrend if CrossUp(MA_fast, MA_slow): # retracement started swing_high, swing_low = find_last_swing_down() fib = calc_fibo(swing_high, swing_low) place_pending_sell(price=fib[0.382], sl=fib[0.786], tp=fib[0])

The latency arbitrage masking strategy’s role as a masking layer

5.1 Behavioral “normalization”

- Arbitrage yields short-lived trades with machine-like timing.

- MA+Fibo adds natural delays (waiting for pullback), limit entries, wider SL/TP ranges, and execution uncertainty (not all limits get filled).

At the account level this produces:

- trades of different nature (some “high-speed,” some “market-style”),

- diverse holding-time profiles,

- asymmetric PnL distribution (limit trades have different RR than arbitrage).

5.2 Synchronization with Phantom Drift

- No hard links on entry triggers: MA+Fibo reacts to price structure; Phantom Drift reacts to speed/flow differentials.

- Layer config should include:

- max simultaneous positions cap (avoid a “stack” of measurements),

- separate strategy IDs and log tags,

- arbitrage priority on news/spikes; MA+Fibo works “in the background” during calmer trending segments.

5.3 Execution nuances

- Limits at 0.382/0.5 may never fill—this is good (adds naturalism).

- On deep pullbacks to 0.618+, the default is not to chase, to avoid inflating the risk footprint. A dedicated Recovery mode is possible, but it’s a different behavioral pattern and should be rare.

Risk management and exposure control

- Fixed per-trade risk: Recommend fixing risk as a % of equity (e.g., 0.25–0.5% per MA+Fibo trade) so the masking layer doesn’t compete with arbitrage for risk budget.

- RR profile: At 0.382 entries with SL beyond 0.786, RR often lands around 1:1+ aiming to 0.0; with 1.618 extension, 1:1.5–1:2.5 depending on impulse geometry.

- Limit concurrent orders: No more than 1–2 per symbol, and a global N per account—so as not to “drown out” arbitrage.

- Session limits: Fix activity windows (e.g., London/New York)—so the strategy looks like it’s aligned with liquid hours.

- Slippage and fees: MA+Fibo uses limit orders, so slippage is minimal. Still monitor spreads: if spread exceeds k × ATR_tick, do not place orders (MaxSpreadATR parameter).

Impulse & swing “quality” detection (considered for future phases)

A robust find_last_swing_up/down() matters more than it seems:

- Use a zigzag rule (e.g., filters for Depth/Deviation/Backstep) or local extremes confirmed by n bars on both sides.

- Exclude news “spikes” (bar exclusion if High–Low > K×ATR).

- On H1/H4, 2–3 local waves back are enough; don’t build Fibo on overly long history.

Order-management options

- Single limit at 0.382: most conservative.

- Split 50/50 at 0.382 and 0.5: increases partial fills and risk distribution.

- Ladder 0.382/0.5/0.618 with decreasing size: can look “too perfect”; better avoid auto-ladders—two levels are enough.

Stop: baseline beyond 0.786, or beyond the extreme + BufferATR (e.g., 0.5×ATR on H1). Take: conservative → 0.0; aggressive → 1.618 (extension). Partial close example: 50% at 0.0, remainder via trailing on MA_fast or Parabolic SAR (note: SAR shifts the behavioral profile—use carefully).

Environmental filters (optional but useful)

- ADX(14) > 20/25: only take trend trades.

- ATR volatility filter: if ATR < MinATR, the market is “thin”—skip placing limits.

- Calendar filter: no new limits N minutes before/after news (arbitrage is active/priority then).

- Spread filter: Spread ≤ MaxPoints.

- Collision cleanup: if an arbitrage position is already open in the same direction and symbol—either skip the limit or reduce its size.

Arbitrage Masking Strategy Implementation — unified logic

Architecture layers:

- Market State Module: EMA(20/100), ADX, ATR, spread, sessions.

- Swing & Fibo Module: last-impulse detection, level construction, impulse “quality” validation.

- Order Planner: generation of limit orders with SL/TP and time-to-live (TTL) (e.g., cancel after X bars).

- Risk Module: fixed-risk sizing, total exposure cap, fee accounting.

- Integration Layer: signal routing, Phantom Drift priority, unique tags, logging.

Practical tips:

- In SharpTrader, expose parameters in Settings (including UseADX, UseSessionFilter, SplitEntry, etc.).

- Avoid unnecessary engine refreshes and respect TTL if price moves away without retest.

- In FIX connectors, control TimeInForce (GTC/Day) and map stop-limit/limit properly to the venue.

- Testing and validation as a masking layer

The test goal is not “max profit,” but to:

- demonstrate stable, modestly positive or near-flat returns at low risk;

- verify that holding time and trade-size distributions blend well with arbitrage;

- assess broker visibility: entry frequencies, session timing, stop/take magnitudes.

Metrics:

- WinRate, Profit Factor, average/median holding time, average/max adverse excursion.

- Separate reports by sessions and by symbols.

- Count of unfilled limit orders (a plus for naturalism).

- Stitched report with arbitrage: combined account profile before/after adding the masking layer.

Symbols & TFs:

- Classics: EURUSD, GBPUSD, USDJPY, metals XAUUSD, indices US100/US30/DAX.

- Timeframes: H1/H4 (M15 intraday is possible but weaker masking—too frequent and granular).

- Managing collisions with arbitrage

- Priority: during news and volatility spikes, arbitrage first.

- Per-symbol limits: if the arbi module already holds a position, MA+Fibo may skip the setup or use smaller size.

- Hedging logic (optional): avoid automatic cross-hedging between modules to prevent an internal “algo tug-of-war.”

Preventing latency arbitrage “recognizable” patterns

To avoid creating a new, detectable “masking profile”:

- Randomize TTL of limits (e.g., 3–7 bars).

- Randomize splits between 0.382 and 0.5 (e.g., 40/60, 60/40, 50/50).

- Apply micro-jitter to SL/TP (±0.1–0.2×ATR) within reason.

- Schedule occasional pause days for filters (e.g., one no-MA+Fibo day per week).

- Slightly vary time windows; not always the textbook “trend hours.”

Typical scenarios and case notes

- Strong trend without a 0.382 retest: limits don’t fill → no problem. The next impulse will form a new swing and levels.

- Deep correction to 0.618–0.786: default is not to chase. If a Recovery mode is used, keep it rare and strictly bounded.

- Range/ADX < 20: there will be no orders—by design.

- Wide spreads/night/Asian session: filters disable order placement.

- Big news spike: ATR bar exclusion—MA+Fibo stands down while arbitrage operates.

Tuning for different instrument classes

- FX majors: EMA(20/100), ADX > 20, split entries 0.382/0.5; SL beyond 0.786 + 0.5×ATR; partial TP at 0.0, remainder trailing.

- Gold (XAUUSD): higher volatility—raise MinATR, widen buffers beyond extremes, reduce position size.

- Indices (US100/US30/DAX): prefer H1/H4, stricter “large-bar” filter (e.g., > 1.5×ATR), exclude news.

- Crypto (BTC/ETH): 24/7 and noisy—apply strict spread/volatility limits; consider 0.5-only entry.

Logging and monitoring (for masking audit)

- Log: time of limit placement and fill, rationale (swing ID, Fibo levels), EMA/ADX/ATR, spread, TTL.

- Maintain separate per-strategy reports (arbitrage vs. MA+Fibo) and a combined view.

- Weekly controls: rolling PF, average duration, % unfilled limits, TTL cancels.

- Keep behavioral charts: entry-time histograms, holding-time distributions, SL/TP heatmaps.

Practical integration with Phantom Drift Arbitrage Strategy

- Initial priority: Phantom Drift = primary, MA+Fibo = secondary.

- Risk split: e.g., arbitrage 70–90% of risk budget, masking 10–30%.

- Module communication: via a central router that knows active positions and decides whether MA+Fibo may engage.

- “Quiet days” scenario: when arbitrage is inactive, MA+Fibo keeps the account “breathing” with a sensible flow of “ordinary” trades.

Extensions and evolution

- Adaptive Fibo entry based on current ATR/volatility: prefer 0.5 in high vol, 0.382 in moderate vol.

- Hybrid TP: 0.0 plus trailing on MA_fast or Keltner Channel.

- “Demo-Noise” mode: more frequent, tiny-size limits for behavioral tests with minimal risk.

- Multi-symbol constraint: cap the number of active symbols so the account doesn’t look like a basket of systematic signals.

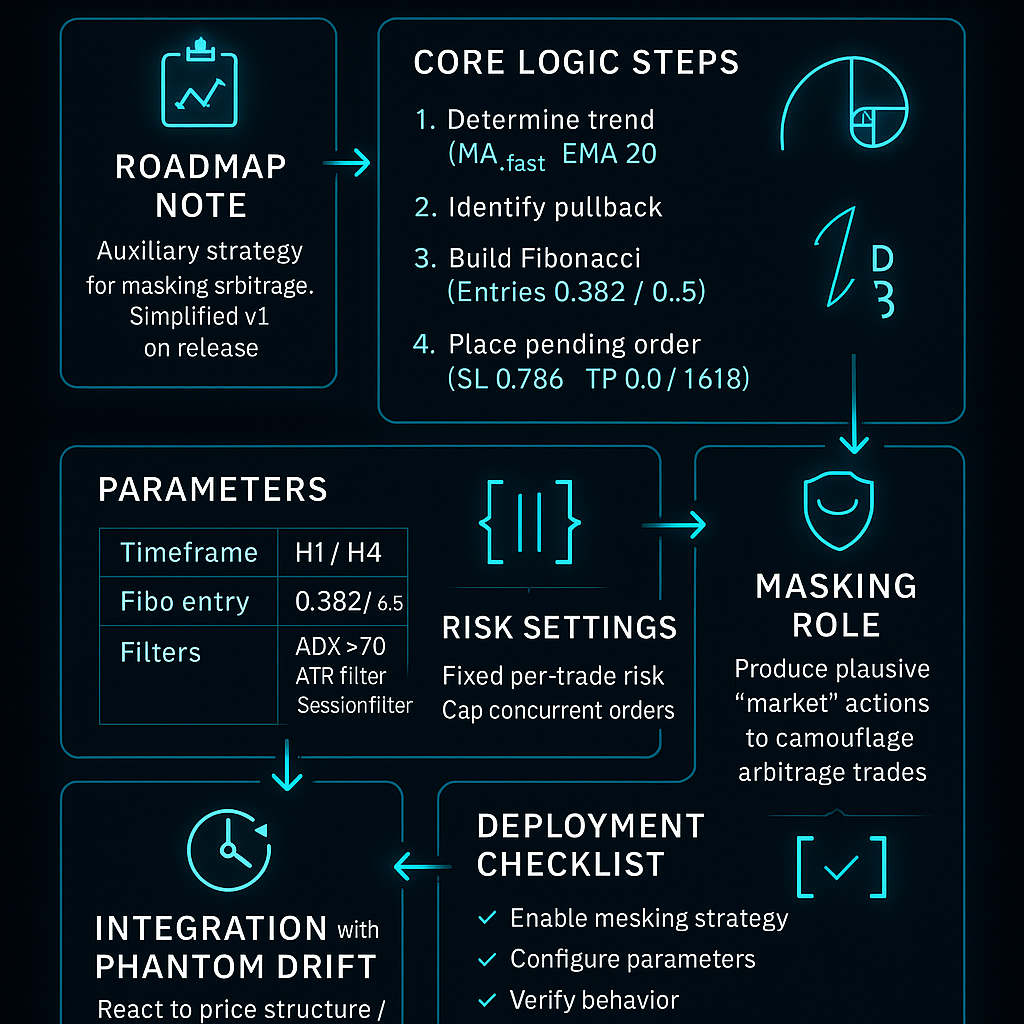

Pic. 2 – Combining trading strategies in the SharpTrader

Pic. 2 – Combining trading strategies in the SharpTrader

Deployment checklist

- Enable the MA+Fibo module as a secondary strategy with a separate strategyId/magic.

- Choose symbols and TFs (H1/H4); configure ADX/ATR/spread/session filters.

- Validate find_last_swing_* on history (excluding “spikes”).

- Set per-trade risk ≤ 0.5%; cap concurrent positions.

- Turn on TTL and 0.382/0.5 split randomization.

- Test standalone logs and combined reports with arbitrage.

- On live, start with micro-lots/micro-risk; verify execution/behavior.

- Review behavioral metrics weekly and refine filters.

Bottom line

The proposed MA trend + Fibo pullback is a strictly auxiliary strategy. Its strength is not aggressive profit extraction, but the formation of a realistic market behavior on the account: sensible limit entries on pullbacks in the trend direction, moderate stops, and natural takes. Combined with Phantom Drift (or another arbitrage logic), it creates a multi-modal profile—some trades “smart and fast,” others “classical and trend-based.” Such a profile is harder for anti-arbitrage systems to evaluate and passes human broker reviews more smoothly. With careful filtering (ADX, ATR, spread, sessions), conservative risk, small randomizations, and disciplined TTL/cancellation rules, you get masking noise with positive expectancy that does not interfere with arbitrage but makes the account’s behavior plausible and lifelike.

FAQ — Hybrid Masking Strategy MA + Fibonacci

What is the main purpose of the MA + Fibonacci strategy?

Does this strategy generate profit on its own?

How does it interact with Phantom Drift?

Which instruments and timeframes are recommended?

Can parameters be customized or extended with AI tools?

How does the strategy improve account camouflage?

What’s the current development stage?