Deutsch

Deutsch 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

Latency Arbitrage and News Trading: Two Powerful Strategies Explained Tuesday May 27th, 2025 – Posted in: Arbitrage Software, News Trading Software

In today’s high-frequency trading environment, success often depends on fractions of a second. Traders who exploit structural inefficiencies and leverage technological advantages become predators in the financial markets. In this article, we’ll explore two advanced approaches — latency arbitrage and news trading — explaining their mechanics, advantages, drawbacks, and who they are best suited for.

What is Latency Arbitrage?

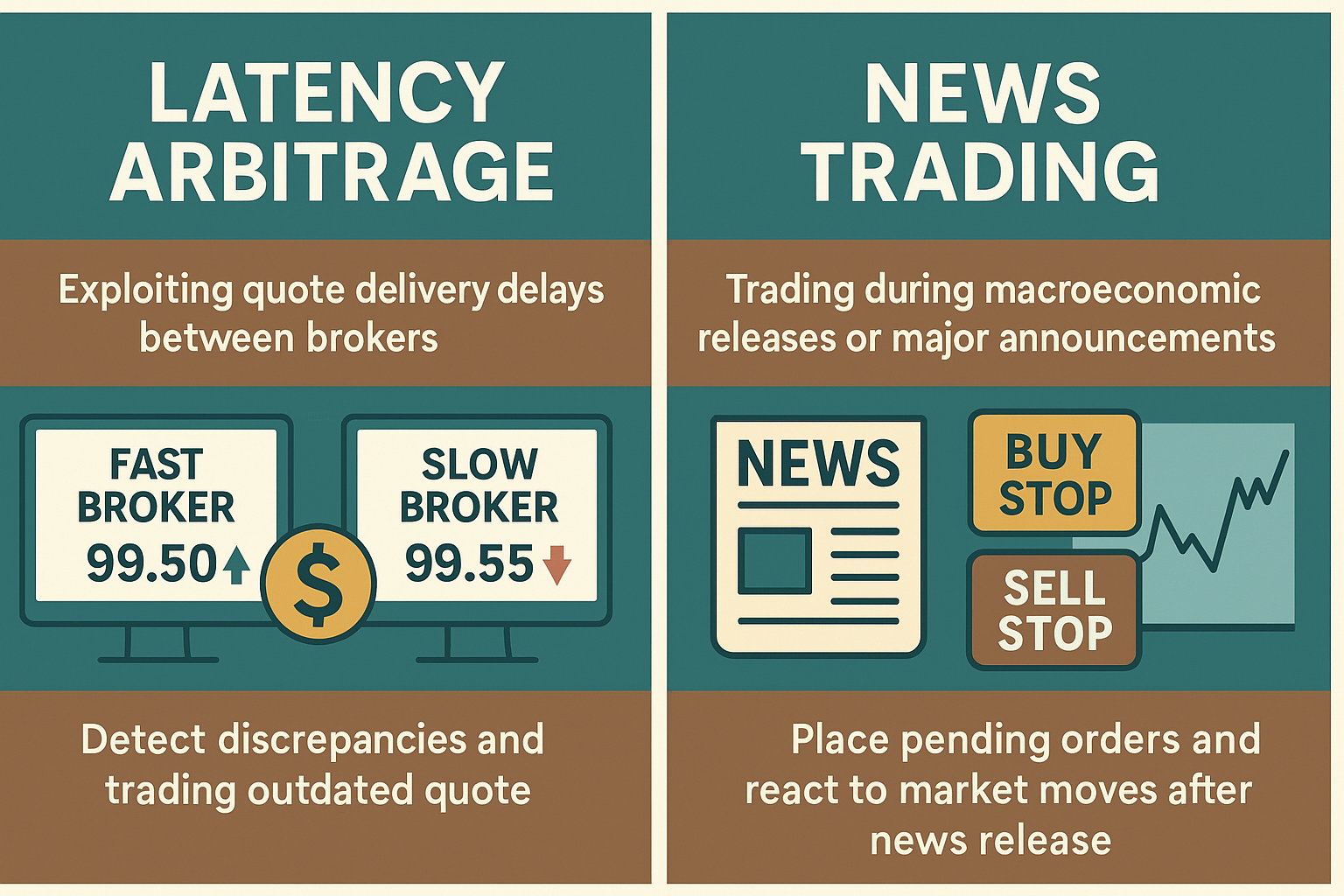

Latency arbitrage is a strategy that exploits quote delivery delays between different brokers or trading platforms. The concept is simple: if one source (a “fast broker”) updates prices faster than another (“slow broker”), the trader can execute trades on the slow broker at a price that is already outdated.

How it works:

- The trader is connected to at least two brokers — one with low-latency access (e.g., via FIX API), the other with a standard trading platform.

- The system monitors real-time quote feeds and compares them.

- When a price discrepancy occurs within a profitable “arbitrage window,” a trade is executed on the slow broker.

- The position is quickly closed once the slow broker’s price catches up.

Advantages:

- Potentially high returns with low per-trade risk (if the infrastructure is well optimized).

- No market analysis required — purely technical.

- Highly automatable with millisecond-level execution.

Drawbacks:

- Requires access to low-latency data sources, often through FIX API or direct market access.

- Some brokers actively defend against arbitrage via plugins, delays, or outright bans. How to choose a broker for arbitrage.

- Significant infrastructure required: co-location, dedicated VPS, or fiber connectivity. Choosing the right VPS for latency arbitrage

What is News Trading?

News trading is a strategy where trades are executed during macroeconomic releases or major political announcements that have the potential to move markets significantly. Learn more about automatic economic news trading software.

How it works:

- The trader receives a machine-readable news feed from providers like Bloomberg, AlphaFlash, or Refinitiv.

- Milliseconds before the news is published, the trader places pending buy and sell stop orders near the current price.

- Once the market reacts, one order is triggered and hopefully earns profit from the resulting movement.

- The other order may hit its stop or receive a margin call, depending on the setup.

Advantages:

- Opportunity for large, fast profits in seconds.

- Highly effective if systems are optimized for speed and accuracy.

Drawbacks:

- High risk of slippage — orders may be filled at worse prices than expected.

- Requires ultra-low latency infrastructure and instant execution logic.

- Some brokers impose restrictions during major events (widening spreads, execution delays, etc.).

Latency Feed vs News Feed: What’s the Difference?

Both strategies require instant access to data, but the type of data and how it’s used differs significantly.

Fast Feed for Latency Arbitrage:

- Market price feeds from brokers or liquidity providers.

- Purpose: detect real-time pricing mismatches between sources.

- Delivered via FIX API, DMA, or even UDP multicast (e.g., CME MDP 3.0).

- Used to make trading decisions based on price latency.

Fast Feed for News Trading:

- Machine-readable economic data feeds (e.g., GDP, NFP, CPI releases).

- Delivered via Bloomberg B-Pipe, AlphaFlash, or Newsquawk feeds.

- Purpose: react within milliseconds to unexpected or impactful macroeconomic data.

- Requires parsing of JSON/XML packets and execution logic.

Comparison Table:

| Feature | Latency Arbitrage | News Trading |

|---|---|---|

| Feed Type | Real-time bid/ask quotes | Machine-readable economic data |

| Data Source | Liquidity providers, brokers, exchanges | News providers (AlphaFlash, Bloomberg) |

| Goal | Exploit price delays | Exploit macroeconomic surprise moves |

| Execution Logic | Compare and trade price mismatches | React to news value with pending or instant orders |

Trade Frequency and Lot Size

Latency arbitrage is a high-frequency strategy. Complete guide to Latency Arbitrage. A trading system can execute dozens or even hundreds of trades daily, each aiming for small profits (often just a few points), but the cumulative gains add up over many trades.

- Average trades: 20–100+ per day

- Lot size: small to moderate

- Approach: rely on statistical edge and scale

News trading is more rare but powerful. Only a few major events per week are worth trading — for example, central bank rates, NFP, CPI, etc. Traders aim to capitalize on big moves with larger position sizes.

- Average trades: 3–10 per week

- Lot size: large, high exposure per trade

- Approach: precision attack on key moments

Comparison:

| Parameter | Latency Arbitrage | News Trading |

|---|---|---|

| Trade Frequency | 20–100+ per day | 3–10 per week |

| Lot Size | Small / Medium | Large |

| Time in Market | Milliseconds to seconds | Seconds to minutes |

| Trade Preparation | Fully automated | Pre-event analysis and setup |

Camouflage Techniques in Both Strategies

Despite being very different in their execution logic, both latency arbitrage and news trading often require similar camouflage techniques to avoid detection and restriction by brokers. While not all brokers treat news trading as toxic, arbitrage is often blacklisted. Traders use masking methods to disguise their strategies.

Common methods include:

- Pre-positioning / Locking orders before the signal triggers, allowing instant execution while minimizing detection risk.

- Simulating beginner behavior by mixing in random delays, alternating order types, executing trades at varied times, and including some losing trades to appear more “human.”

- Distributing trades across multiple accounts or IPs to avoid statistical profiling and flagging.

- Maintaining secondary accounts with standard or even losing trades to build broker trust.

These techniques are detailed in the article Nuances of Arbitrage Trading, which explains how to avoid being flagged while maximizing profit opportunities.

Even though many brokers do not consider news trading as toxic as arbitrage, during high-impact releases, they may still apply slippage, wider spreads, or delay execution. Masking becomes important when trading with large volumes or high precision.

Conclusion

Both latency arbitrage and news trading are powerful tools in the hands of experienced traders. The former relies on speed and data flow discrepancies, while the latter hinges on reacting to critical economic events. While their execution differs, both require robust infrastructure, careful planning, and, often, stealth.

If you’re a beginner, it’s wise to test both strategies on demo accounts first and work with reliable brokers. If you’re experienced, integrating these techniques into your system can give you a distinct edge over the competition.

📌 FAQ: Latency Arbitrage and News Trading

❓ What is the main difference between latency arbitrage and news trading?

Latency arbitrage relies on differences in price updates between brokers due to data transmission delays. It’s technical and automated.

News trading capitalizes on sharp market moves caused by economic announcements. It’s event-driven and usually less frequent but more aggressive.

❓ Do both strategies require low-latency infrastructure?

Yes. Both strategies depend on speed:

-

Latency arbitrage demands ultra-fast quote comparison tools (e.g., FIX API, co-located servers).

-

News trading requires instant access to machine-readable news feeds and the ability to react within milliseconds.

❓ How many trades can I expect from each strategy?

-

Latency arbitrage: 20–100+ trades per day, each seeking a small price differential.

-

News trading: 3–10 trades per week, usually around major macroeconomic releases.

❓ Are these strategies considered “toxic” by brokers?

Latency arbitrage is often considered toxic by brokers and may trigger restrictions or trade rejections.

News trading is generally tolerated, but brokers might still impose wider spreads, slippage, or execution delays during high-impact events.

❓ Can I use both strategies at the same time?

Absolutely — in fact, advanced traders often combine both to diversify opportunities and balance risk. This hybrid approach requires robust infrastructure and careful execution timing.

❓ What is “masking” in the context of these strategies?

Masking refers to techniques used to hide your strategy from the broker, such as:

-

Locking trades before the actual signal.

-

Mimicking inexperienced trading behavior.

-

Spreading orders across accounts.

These help avoid being flagged as a high-risk or toxic trader.

❓ Is it possible to automate these strategies?

Yes. Both latency arbitrage and news trading are well-suited for algorithmic execution, though the automation logic and data feeds differ:

-

Arbitrage bots rely on real-time quote comparison.

-

News bots react to parsed economic data releases.

❓ What’s the best way to start?

-

Test both strategies on demo accounts.

-

Secure access to reliable low-latency data feeds.

-

Choose brokers that tolerate or ignore latency-sensitive strategies.

-

Use professional tools like those offered by BJF Trading Group, which specialize in news trading, arbitrage, and masking automation.