English

English Deutsch

Deutsch العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

外国為替裁定取引の長期的安定性を確保する:ゲーム理論の枠組み 2025年07月15日 – Posted in: Arbitrage Software, Forex trading

はじめに

現在の外国為替市場構造では、あらゆる規模のブローカーが多様なトレーダーのコミュニティにサービスを提供しています。その中には伝統的な戦略を支持する者や、外国為替裁定取引およびレイテンシー裁定取引の手法を用いる参加者も含まれます。私たちは、当社の専門的なソリューションを購入するトレーダーに対し、特に外国為替裁定取引、特にレイテンシー裁定取引の条件が最も有利なブローカーを正確に推奨するという独自の立場を占めています。

しかし、この裁定取引エコシステムの安定性は、プラットフォーム上で不均衡が生じた場合に脅かされます。レイテンシー裁定取引者の数が急激に増加したり、個々の参加者が過度に大きな預金額や増大する注文量で取引を始めたりすると、その状況に対応するためにブローカーはしばしば注文執行の遅延や内部処理手順の変更を余儀なくされます。これにより外国為替裁定取引戦略の効果が低下し、その悪影響は他の取引スタイルを用いるトレーダーにも広がります。最終的に、執行時間の増加やスリッページの発生によって、新規および既存の顧客に対する魅力を失い、ブローカー自身の競争力も損なわれます。

すべての市場参加者にとって自然に浮かぶ疑問は、いかにして長期的な安定性を確保し、外国為替裁定取引トレーダーやレイテンシー裁定取引の専門家、その他市場関係者にとって利益を生む機会を守るか、ということです。本記事では、この問題を有限の資源と相反する利益の下で様々なプレイヤーの戦略的行動を分析する科学的学問であるゲーム理論の視点から考察します。なぜ節度と協力が短期的な利益最大化よりも良い結果をもたらすのか、そしてトレーダーがどのように行動を形成し、共通の利益と自己の利益の双方を得るかを説明します。

ゲーム理論の紹介:個人の利益と集団の結果

ゲーム理論は応用数学の一分野であり、各参加者の結果が自らの決定だけでなく他者の選択にも依存する状況における戦略的行動を研究します。金融市場、特に外国為替裁定取引やレイテンシー裁定取引の文脈では、個々の利益と集団の福祉の間に緊張が生まれます。トレーダー、ブローカー、およびその他の参加者は、限られた執行能力と相反する利害のもとで日々意思決定を行い、複雑な相互作用のダイナミクスを生み出しています。

古典的な例が囚人のジレンマです。二人の容疑者は独立して協力(黙秘)するか、裏切り(自白)するかを選択します。裏切りは相手の選択に関わらず個人的な利益をもたらしますが、両者が裏切ると協力した場合より悪い結果になります。個々の合理的な選択が非効率な集団的結果につながるのです。

このジレンマは外国為替裁定取引における重要な問題を反映しています。レイテンシー裁定取引者が最大の取引量を追求すると、市場全体の執行品質を低下させ、全参加者に悪影響を及ぼします。このパラダイムの理解は効果的な戦略的意思決定に不可欠です。

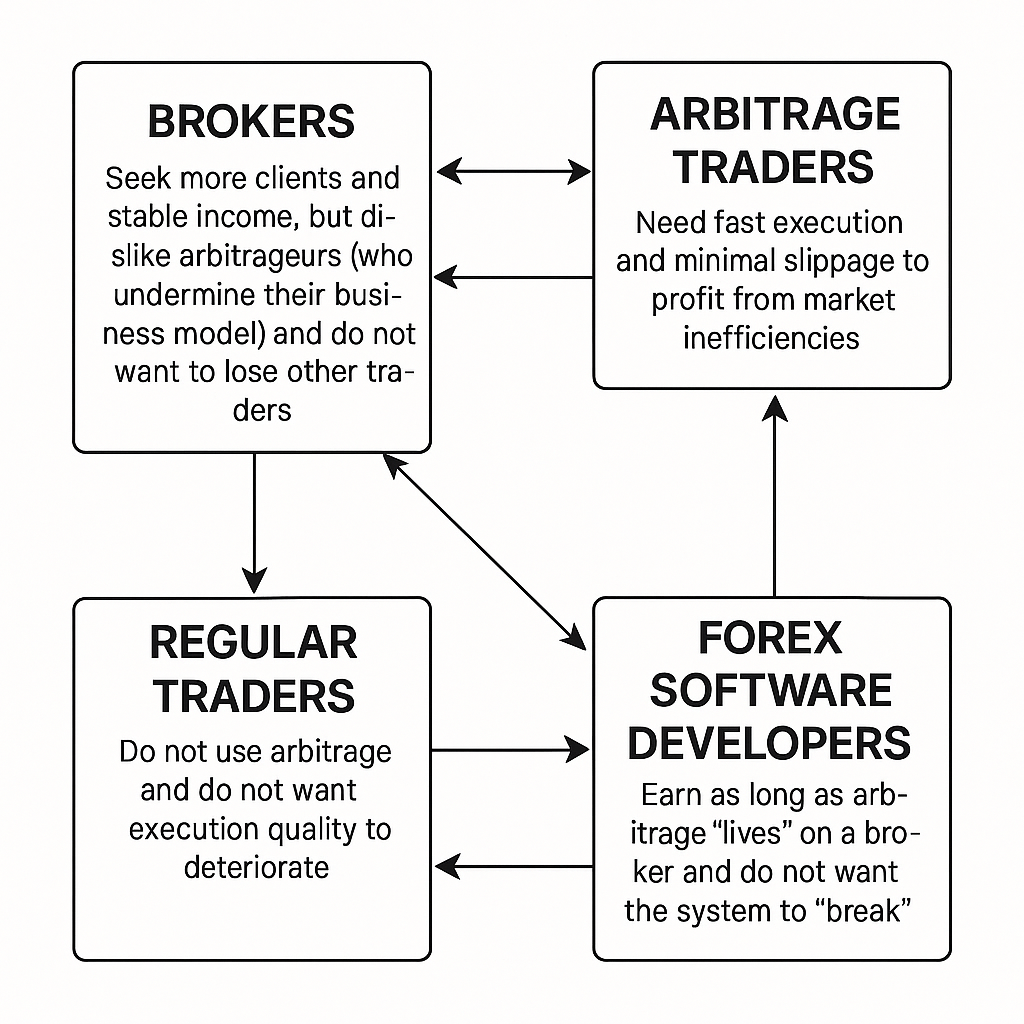

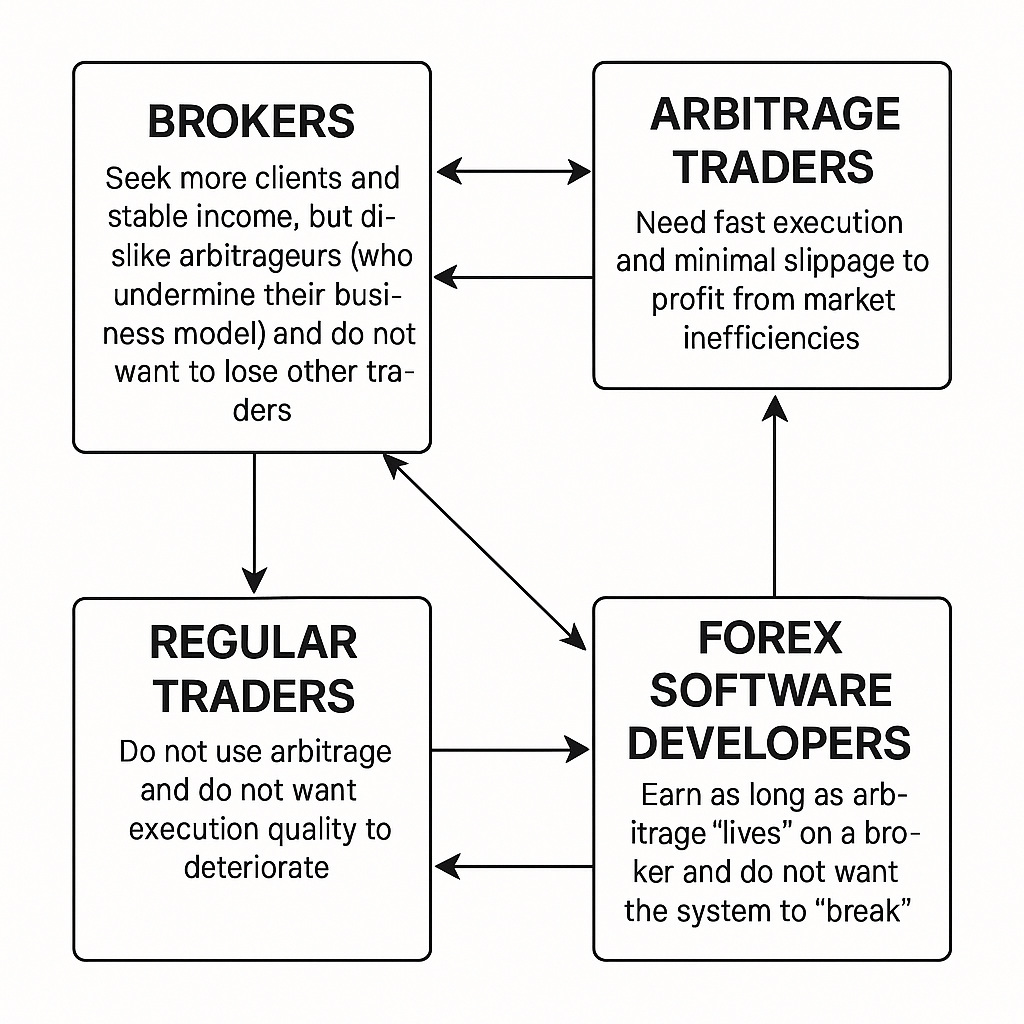

プレイヤーと利害関係の形式化

-

ブローカー – より多くの顧客と安定収入を求めるが、ビジネスモデルを損なう可能性のある裁定取引者を嫌い、通常のトレーダーを失いたくない。

-

裁定取引トレーダー – 特にレイテンシー裁定の専門家は、儚い市場の非効率から利益を得るために高速な執行と最小限のスリッページを必要とする。

-

通常のトレーダー – 裁定取引を使わず、執行品質の悪化を望まない。

-

外国為替ソフトウェア開発者 – 裁定取引がブローカー上で存続している限り収益を得ており、システムが「壊れる」ことを望まない。

問題の説明

-

裁定取引量が少ない場合、ブローカーはそれを容認します:執行は速く、スリッページは最小限であり、外国為替裁定取引は「金のなる木」として機能します。

-

レイテンシー裁定取引の活動が増加すると(トレーダーが増えるか、ボリュームが大きくなる)、執行は遅くなりスリッページは増加します。ブローカーは条件を厳しくし、すべてのトレーダーグループが影響を受けます。

-

長期的には、ブローカーは裁定取引者と通常トレーダーの両方を失い、新規顧客にとって魅力がなくなります。

-

共有資源の悲劇(Tragedy of the Commons):新たな裁定取引者は「できるだけ多くを取ろう」とし、共有資源(執行能力)が枯渇します。

例え話:共通の牧草地と羊

共通の牧草地(執行能力)があり、羊は裁定取引の取引を表します。羊が少数だけ草を食べれば草は育ち、みんなが満足します。羊が多すぎると草が踏み荒らされ、どのグループにも十分ではなくなります。

目標:持続可能なエコシステムの構築

ゲーム理論の視点から解決策を検討します:

裁定取引の割当・制限

- 裁定取引トレーダーの数や、1人あたりの日次取引量(例:1日あたりXロットまで)に制限を設ける。

- 「招待制」「ホワイトリスト」または紹介管理によって実装し、招待されたトレーダーのみが裁定取引を利用できる。

- 利点:裁定取引が長く続き、執行品質が保たれ、ブローカーが満足する。

- 欠点:スケールしにくく、誰が招待されるかの問題が生じる。

ブローカーの差別化

- 負荷分散のために異なるブローカーを裁定取引者に推奨し、特定のブローカーの過負荷を防ぐ。

- トレーダーを定期的にブローカー間でローテーションする。

柔軟な推奨(スマート割当)

- 各ブローカーの執行統計をリアルタイムで追跡する。

- ブローカーの執行品質が低下したら、新規クライアントを他のブローカーへ誘導する。

- 利点:どのブローカーも完全に機能停止せず「新鮮さ」を保つ。

- ホワイトラベルやパートナーシステムで自動化可能。

トレーダーの行動規範

- 顧客教育:「大きな預金から始めない」「取引量を分割する」「ピーク時間帯の裁定取引を避ける」など。

- 過負荷リスクを説明する初心者向けガイドの提供。

モニタリングツール

- 執行時間、遅延、スリッページ、取引量のデータを継続的に収集する。

- 執行時間が急上昇した際に、自動で該当ブローカーの新規クライアント制限を警告する。

追加手段

- トレーダーブレンド:裁定取引者と通常トレーダーを組み合わせて自然な負荷隠蔽を促進する。

- テスト「レイド」:小規模な裁定取引波を送信し、ブローカーの反応を調査、推奨を動的に調整する。

- ブラックリスト:執行品質が閾値を下回った場合、回復まで推奨から除外する。

ゲーム理論的説明

- これは有限資源を扱う動的反復ゲームである。

- 目標は短期的な利益最大化ではなく、執行能力の長期的かつ持続可能な配分である。

- 均衡は自制と協力によって生まれ、「みんなが少しずつ取れば全員が勝つ」。

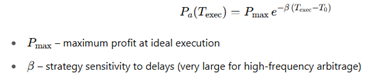

執行品質劣化の数学モデル

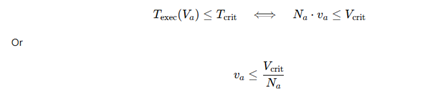

裁定取引フロー Va に対する執行時間のモデルは以下の通り:

執行に対する裁定取引者の利益

利益を以下とする:

システムをゲームとして考える

システムに新規の裁定取引者が入ると、他の流量が低ければ利益を得る。しかし、Va > Vcrit になると利益は急激に低下する。

- 誰もが利己的に行動し(自身の取引量 va を最大化すると)、システムは崩壊する。

- va や裁定取引者数 Na の制限による調整が、システムを「緑のゾーン」に長く保つ。

最適化:何人のトレーダーを「投入」できるか?

最大の Na および/または va を見つける条件は以下:

この閾値条件が執行劣化を防止する。

「共有地の悲劇」の数式表現

調整がない場合、各裁定取引者は va を増加させ続け、

– ナッシュ均衡: 他者が増やさなければ自分だけ増やすことは合理的だが、全員が増やせば全員が損をする。

ペナルティや協力の導入

過負荷に対するペナルティを設けることができる:

![]()

ここで S はペナルティ項(例:手数料増加、取引量制限、アカウント停止)であり、これによってナッシュ均衡はペナルティ回避のため協力的行動に整合される。

システムの動態

- 制御なし:執行が制限を超え、裁定取引者が離脱し、ブローカーは全顧客を失う。

- 適切な制御あり:システムは安定し、ブローカーとトレーダーの双方が利益を得て、ブローカーは継続的に推奨可能となる。

可視化

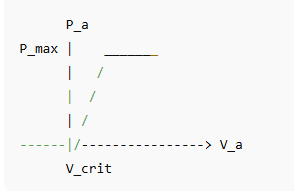

1人の裁定取引者の利益曲線と総裁定取引流量 Va の関係:

Vcritを超えると利益は急落する。

応用例

同じブローカーで2つの裁定取引戦略を比較する:

- 制御された(「穏健な」)戦略:月利30%、長期持続可能な裁定取引

- 攻撃的(「強欲な」)戦略:月利70%、しかし1か月後に執行停止またはアカウント停止

開始資金は2,000ドルとする。

制御戦略(月利30%、8か月間)

攻撃的戦略(月利70%、1か月後停止)

![]()

総利益:3,400ドル − 2,000ドル = 1,400ドル

| 月 | 制御(30%) | 攻撃的(70%) |

| 0 | $2,000 | $2,000 |

| 1 | $2,600 | $3,400 |

| 2 | $3,380 | — |

| … | … | — |

| 8 | $16,315 | — |

グラフの説明:

- 制御戦略:8か月間の安定した指数関数的成長

- 攻撃的戦略:1か月目に急激な上昇、その後停止

穏健な長期戦略は、同じ元本で強欲な戦略の約10倍の利益をもたらし、執行品質とブローカーとの関係を維持します。

結論

本記事では、裁定取引の無秩序な成長が市場参加者全体の執行品質を損ね、時間とともにブローカーの競争力を低下させることを検証しました。ゲーム理論的視点の適用により、個別の裁定取引者による純粋な利益最大化が「共有地の悲劇」を引き起こし、執行能力の過剰搾取と全員の損失に繋がることを示しました。続いて、割当制限、ブローカー差別化、スマート割当、トレーダー行動規範、リアルタイム監視など、個々のインセンティブと集団の利益を調和させる協調的メカニズムを提案しました。数学モデルと実例を通じて、適度で協調的な裁定取引活動がトレーダーの持続的利益、ブローカーの安定収益、ソフトウェアプロバイダーの長期的存続を可能にすることを示しました。最終的に、自己抑制と戦略的協力こそが、積極的な取引量拡大よりも、長期的な利益機会と市場の健全性を維持する最善の道であると結論付けました。

よくある質問

Q1: なぜ裁定取引量の増加が執行品質を損なうのですか?

より多くの裁定取引者と大きな注文量が単一のブローカーのプラットフォームに流入すると、合計の Va が臨界値 Vcrit を超えることがあります。この点を越えると、ブローカーの注文処理能力が過負荷になり、執行時間 Texec が増加し、スリッページが拡大します。遅い約定と広がるスプレッドが全員の収益性を低下させます。

Q2: 外国為替裁定取引における「共有地の悲劇」とは何ですか?

これは、各裁定取引者が自分の取引量を最大化しようと独立して行動し、その結果共有資源であるブローカーの執行品質を集団的に枯渇させる状況を示します。放置すれば、需要が供給を上回り、全参加者の利益とブローカー関係を破壊します。

Q3: ブローカーとトレーダーはどのように協調して執行品質の劣化を防げますか?

協調の形態は多様です:

- 裁定取引者ごとの1日当たりロット数の割当や制限

- 複数の取引所間で負荷を分散するブローカーの差別化

- 執行指標をリアルタイムで監視し、新規顧客を適宜振り分けるスマート割当システム

- 預金や取引量を分散するよう助言する行動規範

Q4: これらの解決策にゲーム理論はどのように関わっていますか?

ゲーム理論はトレーダーとブローカー間の戦略的相互作用を理解するための形式的枠組みを提供します。有限資源を持つ繰り返しゲームとして裁定取引をモデル化することで、執行品質と集団利益を維持する均衡条件(例えば合意された取引量制限)を特定できます。

Q5: 安定した裁定取引量を保証する数学的条件は何ですか?

簡単な必要条件は以下です:

ここで、Na はアクティブな裁定取引者の数、va はトレーダー1人当たりの平均取引量、Vcrit はブローカーの容量閾値です。この制限を超えないことで執行遅延を防ぎます。

Q6: ペナルティやインセンティブはコンプライアンスをどのように改善しますか?

合意された割当を超えたトレーダーに対し、手数料の増加、取引量課金、一時的アカウント停止などのペナルティを課すことで、過負荷のコストを内在化させます。逆に、規則遵守者には優遇価格などのインセンティブを与え、協調的行動を促進します。

Q7: 今日、トレーダーが取るべき実践的なステップは何ですか?

- 透明な執行指標と明確な割当ポリシーを持つブローカーを選ぶ。

- 複数のブローカーやサブアカウントに裁定取引量を分散する。

- 執行時間とスリッページを監視し、流れを動的に調整する準備をする。

- 推奨される「ベストプラクティス」(例:ピーク時間帯の回避、大口入金の分散)を守る。

節度、協力、リアルタイム監視を受け入れることで、トレーダーとブローカーは数週間でシステムを疲弊させるのではなく、数か月にわたり持続可能な裁定取引利益を享受できます。