English

English 日本語

日本語 العربية

العربية 한국어

한국어 Español

Español Português

Português Indonesia

Indonesia Tiếng Việt

Tiếng Việt 中文

中文

Index-Arbitrage: Strategie am Beispiel des US30 Donnerstag, der 10. Juli 2025 – Posted in: Arbitrage Software, News Trading Software – Tags: us30 arbitrage, us30 latency arbitrage

Einleitung

Indizes sind synthetische Instrumente, die die Entwicklung von Gruppen von Aktien oder ganzen Wirtschaftssektoren widerspiegeln. Einer der bei Tradern beliebtesten Indizes ist der US30 (Dow Jones Industrial Average, DJIA), der einen Korb der 30 größten US-Industrieunternehmen abbildet. Aufgrund seiner hohen Liquidität und Empfindlichkeit gegenüber makroökonomischen Nachrichten bietet der US30 eine ausgezeichnete Plattform für die Umsetzung von Arbitragestrategien.

In diesem Artikel behandeln wir:

- Was Indexarbitrage ist

- Welche Arbitragemöglichkeiten es beim US30 gibt

- Die wichtigsten Strategien: Latenzarbitrage, Futures-Arbitrage, Paararbitrage und News-Arbitrage

- Praktische Aspekte und Risiken

-

Latenzarbitrage beim US30

Strategieüberblick:

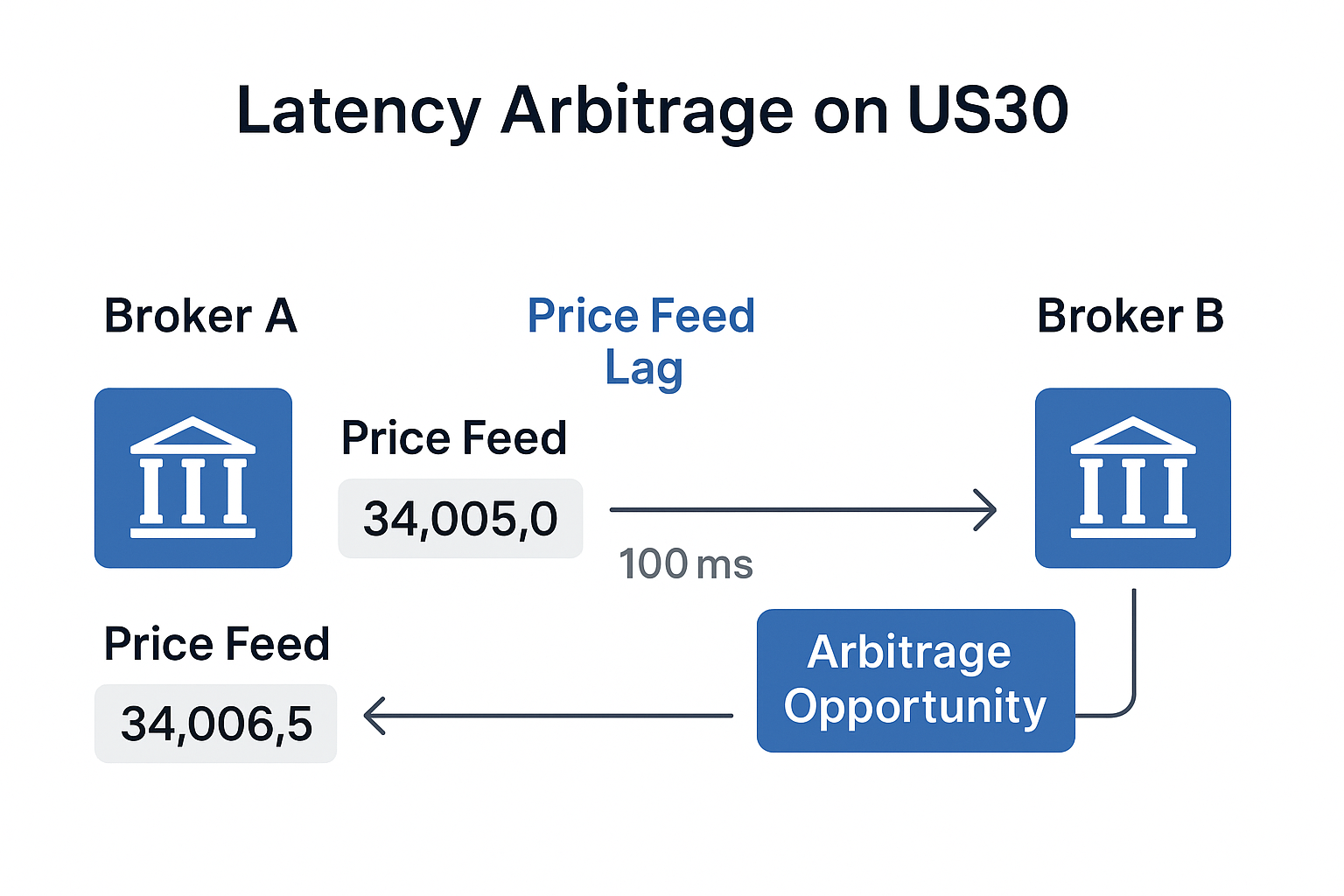

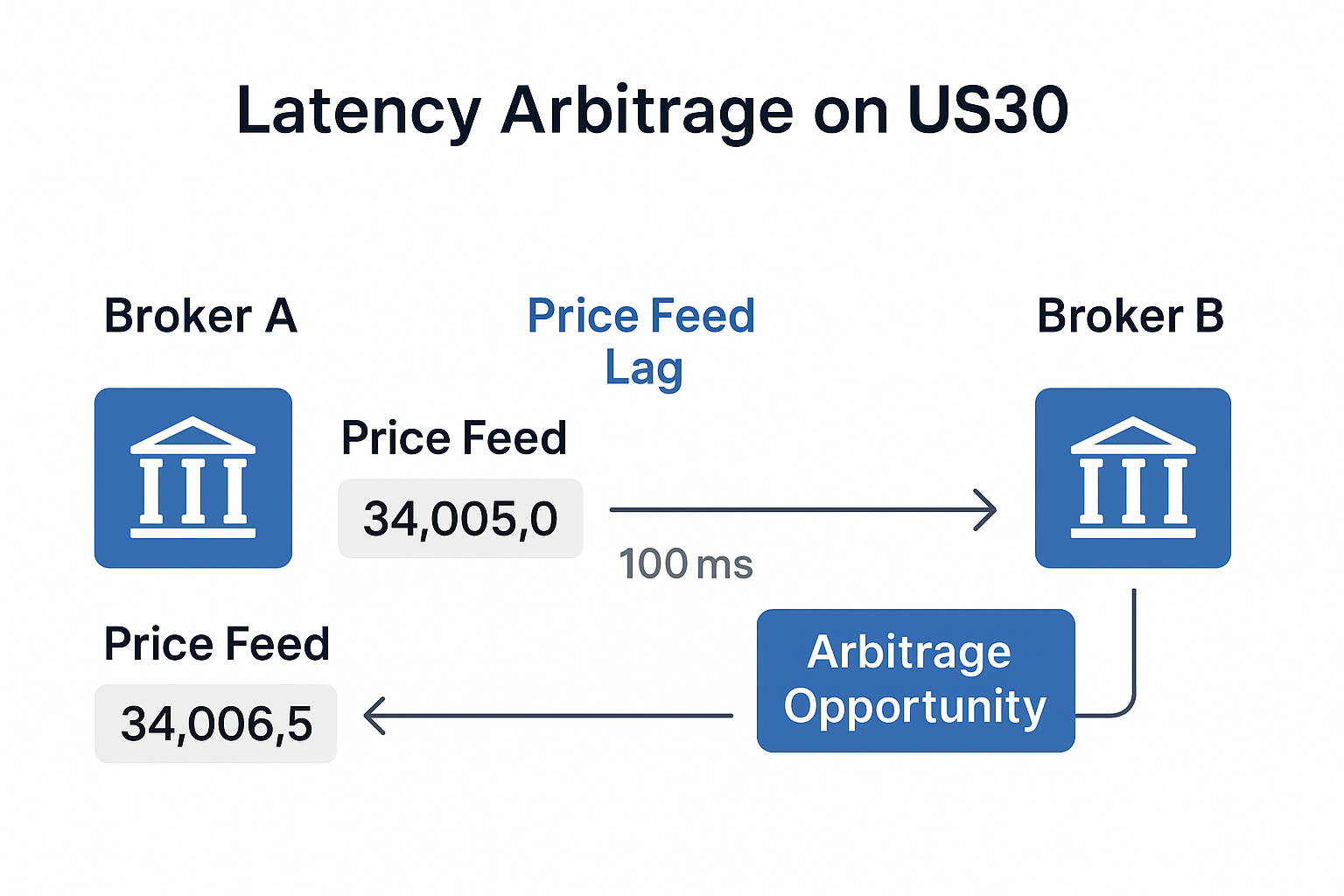

Latenzarbitrage nutzt Verzögerungen bei der Preisaktualisierung zwischen verschiedenen Brokern oder Liquiditätsanbietern, um daraus Gewinn zu ziehen. Dies ist besonders relevant bei hochvolatilen Indizes wie dem US30 (Dow Jones), wo selbst kleine Verzögerungen profitabel genutzt werden können.

Warum funktioniert das beim US30?

- Der US30-Index bewegt sich oft in plötzlichen Schüben, insbesondere während der US-Handelszeit und bei der Veröffentlichung wichtiger makroökonomischer Nachrichten.

- Broker erhalten Kurse aus unterschiedlichen Quellen und aktualisieren diese mit unterschiedlichen Frequenzen und Filtermechanismen.

- Dadurch entsteht ein Preisverzug, bei dem ein Broker bereits eine Marktbewegung abbildet, während ein anderer dies noch nicht getan hat.

Kursabweichungen zwischen Quotes – der entscheidende Faktor

Im Gegensatz zu Währungen haben Index-Kurse (insbesondere US30-CFDs) häufig einen systematischen Versatz zueinander. Das wird verursacht durch:

- Unterschiede bei den Kursquellen (Futures, ETFs, aggregierte Daten)

- Broker-seitige Filterung oder Rundung

- Timing-Unterschiede bei Datenströmen (Quotes durchlaufen eine unterschiedliche Anzahl an Knotenpunkten)

⚠️ Der Versatz ist nicht konstant! Er kann sich mehrmals am Tag ändern – insbesondere bei starken Marktbewegungen, Wechseln in der CME-Handelssitzung oder während Nachrichtenereignissen. Deshalb muss jede Software für Latenzarbitrage auf Indizes eine automatische Neuberechnung des Offsets und eine dynamische Kursanpassung enthalten.

Ohne diese Mechanismen könnte die Strategie einen technischen Offset fälschlich als Arbitragesignal interpretieren.

Besonderheiten der Handelssitzungen

Es ist wichtig zu beachten, dass Indizes – im Gegensatz zu Währungen – nicht rund um die Uhr gehandelt werden. Zum Beispiel:

- US30-CFDs sind etwa von 01:00 bis 23:00 Uhr GMT+2 handelbar, aber außerhalb der US-Handelszeit sinkt die Liquidität stark.

- Echte Dow-Jones-Futures (YM) werden mit Unterbrechungen an der CME gehandelt und weisen Liquiditätsspitzen zum US-Börsenstart und -schluss auf.

Daraus folgt:

- Der Algorithmus muss die aktiven Handelszeiten berücksichtigen,

- Signale außerhalb der liquidesten Phasen herausfiltern,

- Den Handel bei weiten Spreads und geringem Volumen vermeiden.

Fazit: Latenzarbitrage auf dem US30 kann sehr effektiv sein, insbesondere bei der Nutzung institutioneller Echtzeit-Feeds, schneller VPS und einer Multi-Broker-Architektur. Der Schlüssel zum Erfolg liegt in der dynamischen Offset-Anpassung, dem Handel nur während aktiver Sitzungen und dem Verbergen des eigenen Verhaltens, um Broker-Sanktionen zu vermeiden.

-

Arbitrage zwischen Index und Futures

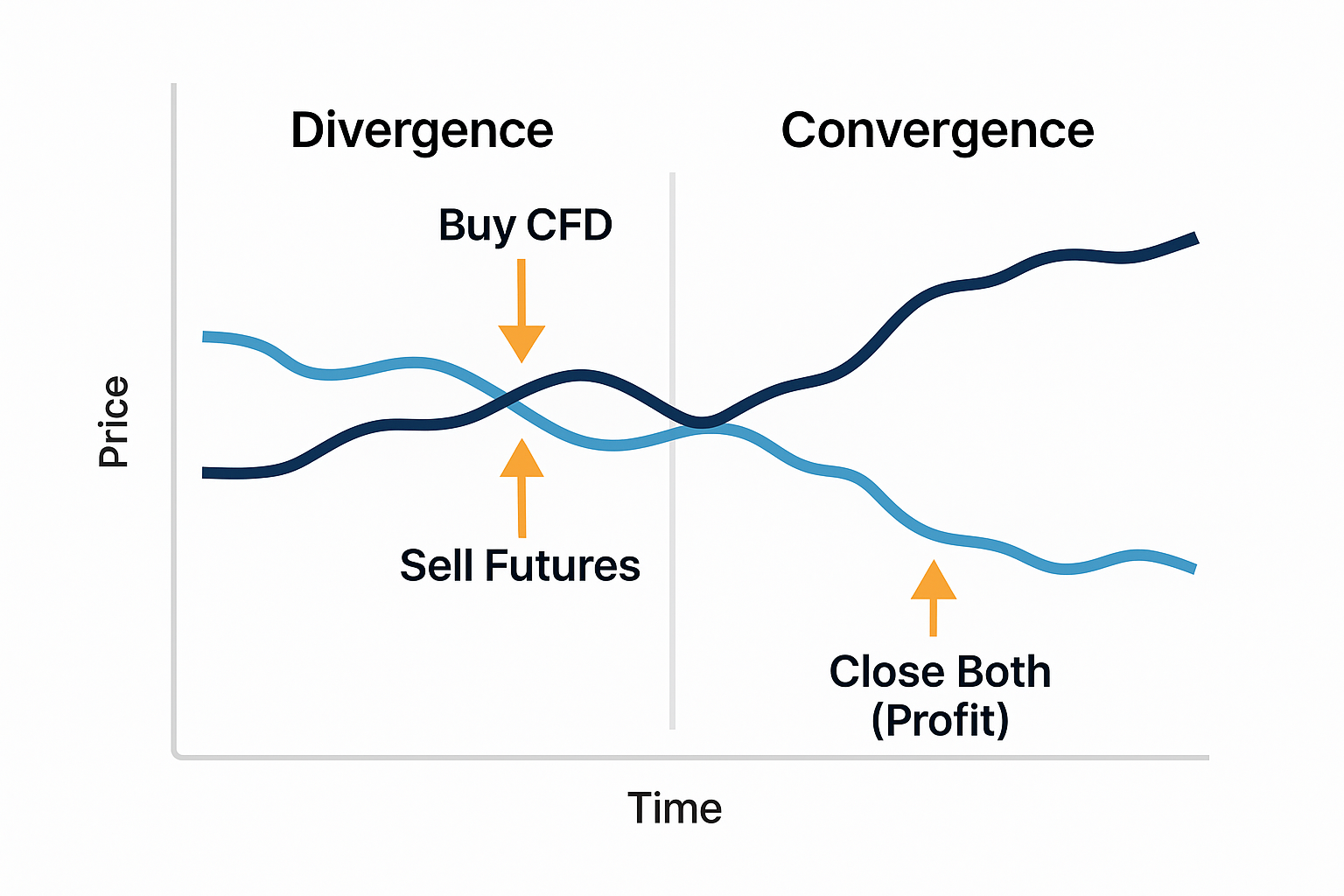

Funktionsweise:

Der DJIA-Future (z. B. YM an der CME) kann sich zeitweise vom CFD-Preis für den US30 bei einem Broker unterscheiden. Diese Abweichungen lassen sich für Arbitrage nutzen:

- Steigt der Future und hat der CFD noch nicht reagiert, kann man den CFD kaufen und den Future verkaufen.

- Die Positionen werden geschlossen, sobald sich das Gleichgewicht wieder einstellt.

Voraussetzungen:

- Zugang zur CME (über Interactive Brokers, NinjaTrader, CQG usw.)

- CFD-Plattform mit schneller Ausführung (z. B. cTrader oder FIX API)

-

Paararbitrage: US30 und andere Indizes

Paararbitrage (statistische Arbitrage oder Pairs Trading) bedeutet das gleichzeitige Handeln zweier historisch korrelierter Indizes oder deren Derivate. Beim US30 (Dow Jones) sind beliebte Paarungen:

- US30 und S&P500 (SPX / US500)

- US30 und NASDAQ100 (NDX / US100)

- US30-CFD und Dow-Future (YM an der CME)

- US30 und ETF DIA

Weicht ein Instrument vorübergehend von der üblichen Beziehung zum anderen ab, kann ein Trader Gegenpositionen eröffnen, in der Erwartung, dass sich die Korrelation wieder einstellt.

Beispiel für die Strategie:

- Historisch verlaufen US30 und S&P500 synchron.

- Irgendwann steigt der S&P500 sprunghaft, aber der US30 nicht.

- Der Trader verkauft den S&P500 und kauft den US30, in der Erwartung, dass der US30 „aufholt“.

Wichtig: Lot- und Kontraktgrößenabgleich

Beim Handel von zwei Indizes ist es entscheidend, die Handelsvolumina korrekt abzustimmen, da:

- Jedes Instrument eine andere Kontraktgröße hat.

- Beispiel:

- US30-CFD bei einem Broker: 1 Lot = 1 $ pro Punkt,

- YM-Future (CME): 5 $ pro Tick, wobei 1 Tick = 1 Punkt ist.

Beispiel für die Anpassung:

Wenn der CFD 1 $/Punkt und der Future 5 $/Punkt ist und Sie das Risiko ausbalancieren wollen, sollten Sie:

- 5 Lots CFD gegen 1 Future-Kontrakt eröffnen.

⚠️ Prüfen Sie vor Start der Strategie immer die Kontraktgröße und die minimalen Lotgrößen beider Instrumente.

Handelssessions beachten

Paararbitrage erfordert, dass beide Instrumente gleichzeitig aktiv und liquide sind. Das ist besonders wichtig, wenn:

- Ein Instrument ein Future (z. B. YM an der CME) ist,

- Das andere ein CFD ist, das beim Retail-Broker 5/24 angeboten wird.

Empfehlung:

- Definieren Sie das Handelsfenster als Schnittmenge beider Sessions.

- Außerhalb dieser Zeiten: keine neuen Trades und ggf. Strategie pausieren.

Swap und Dreifach-Swap

Paartrades werden oft über Nacht gehalten, daher ist es wichtig, die Swap-Gebühren zu kennen, insbesondere:

- Dreifach-Swap wird von Mittwoch auf Donnerstag oder am Freitag berechnet (zum Ausgleich für das Wochenende).

- Wenn eine Position einen negativen Swap hat, kann das Halten zu dieser Zeit den Profit auffressen.

Was tun?

- Bei negativem Swap die Orders vor dem Dreifach-Swap schließen.

- Positionen nach der neuen Abrechnungsperiode auf gleichen Preisniveaus wieder eröffnen.

Fazit:

Paararbitrage auf Indizes erfordert:

- Präzises Positionssizing (Lotgröße, Kontraktgröße),

- Beachtung von Handelssitzungen und Liquidität,

- Überwachung von Swaps, insbesondere Dreifach-Swaps,

- Dynamisches Risikomanagement, insbesondere bei starken Indexabweichungen.

Mit korrektem Setup und regelmäßiger Kalibrierung kann die Strategie auch in Seitwärtsmärkten und unsicheren Zeiten stabile Erträge liefern.

-

Newsbasiertes Trading: Reversal-Strategie beim US30

Der US30-Index ist wie Gold (XAU/USD) äußerst sensibel auf wichtige US-Makrodaten: Non-Farm Payrolls, Verbraucherpreise (CPI), Kern-PCE, Fed-Entscheidungen und andere Schlüsseldaten lösen oft starke Kursbewegungen aus.

In der professionellen News-Arbitrage nutzt man jedoch kein klassisches Ausbruchssystem mit Pending Orders, sondern ein Reversal-Modell – besonders effektiv bei Gold.

Kern der Strategie: Reversal Trading

Anders als bei der klassischen „Newsrichtung“-Strategie werden bei der Reversal-Variante Orders entgegen der Bewegung des Basiswerts eröffnet – basierend auf der Interpretation der Dollarstärke (insbesondere USD).

So funktioniert es in der Praxis:

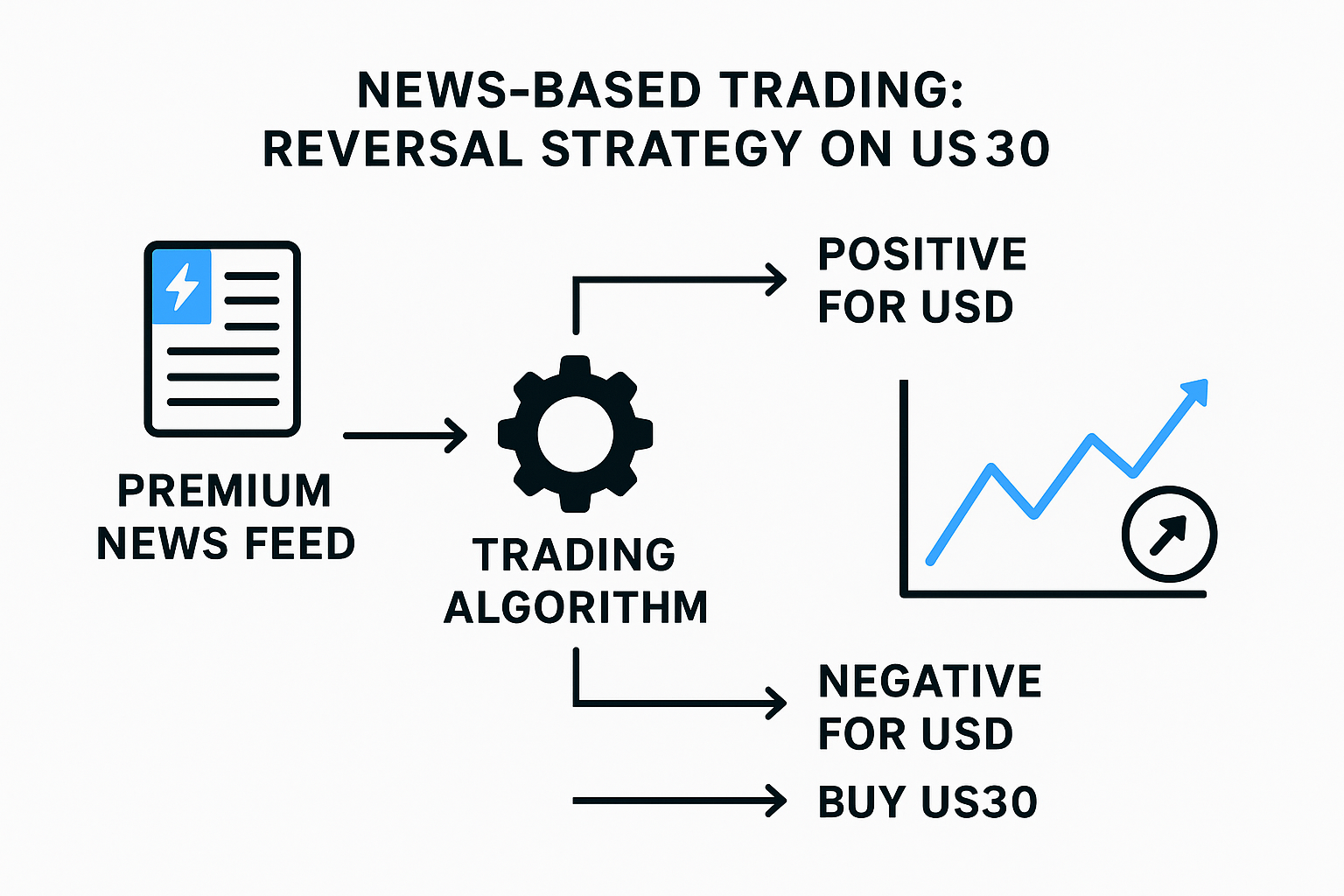

- Wir erhalten die Nachrichten im Voraus von Premium-Aggregatoren wie AlphaFlash, Bloomberg B-Pipe, Need to Know News usw. Diese Anbieter liefern die Daten Millisekunden vor der offiziellen Veröffentlichung.

- Das System entscheidet sofort:

- Ist die Nachricht positiv für den Dollar (USD) → Sell US30 eröffnen

- Ist die Nachricht negativ für den Dollar (oder positiv für Gold) → Buy US30 eröffnen

- Mit anderen Worten: Wir handeln revers auf Grundlage des Nachrichteninhalts:

Gold und Dollar bewegen sich typischerweise gegensätzlich.

Technische Umsetzung:

- Marktorders werden für maximale Geschwindigkeit verwendet.

- Bei FIX API-Execution sind z. B. folgende Ordertypen möglich:

- LimitFoG (Fill or Gap) – Ausführung innerhalb eines bestimmten Bereichs

- LimitEoG (Execute or Gap) – aggressive Limitorder mit erweitertem Slippage

- Jedes Instrument kann genutzt werden, aber US30 (oder XAU/USD) ist besonders geeignet wegen:

- Hoher Liquidität

- Geringen Spreads

- Starker Reaktion auf Fundamentaldaten

Vorteile:

- Früher Zugang zu Informationen: selbst wenige Millisekunden sind entscheidend

- Klare Einstiegslogik: keine Richtungs-Raterei – einfach Nachrichten auswerten und Muster anwenden

- Minimiert die Risiken klassischer Ausbruchsysteme: keine Gefahr von „falschen“ Ausbrüchen, da der Einstieg auf Nachrichteninterpretation basiert, nicht auf der Chartreaktion

Kritische Punkte:

- Erfordert ultraniedrige Latenz (unter 10 ms) vom Nachrichteneingang bis zur Orderplatzierung

- Beste Ergebnisse bei VPS im Broker-Rechenzentrum + FIX API

- News-Parser muss in das Handelssystem integriert sein

- Wichtig: Strategie bei unwichtigen Nachrichten oder hohen Spreads deaktivieren

Beispiel (Non-Farm Payrolls):

- Prognose: +190K

- Tatsächlich: +250K (besser als Prognose → USD steigt)

→ Revers Sell US30 eröffnen (gegen USD)

Fazit

Indexarbitrage, insbesondere auf dem US30 (Dow Jones), bietet erfahrenen Tradern eine Vielzahl an Möglichkeiten, Markteffizienzen auszunutzen. Von Latenzarbitrage, die Millisekunden-Versätze nutzt, über Futures- und Paararbitrage zur Ausnutzung statistischer oder struktureller Fehlbewertungen bis hin zum newsbasierten Trading mit ultraschnellen Datenfeeds – jede Methode erfordert technisches Know-how und ein tiefes Verständnis der Marktstruktur.

Erfolg ist jedoch nicht garantiert. Trader müssen sich ständig an verändernde Offsets anpassen, Kontraktspezifikationen kennen, Handelszeiten überschneiden, Swap- und Liquiditätsrisiken beachten. Strenge Disziplin, zuverlässige Automatisierung und ständige Überwachung sind für nachhaltige Rentabilität unerlässlich.

Mit der richtigen Infrastruktur, Risikomanagement und laufender Kalibrierung kann Indexarbitrage auch in volatilen oder seitwärts tendierenden Märkten einen zuverlässigen Vorteil bieten. Dennoch ist es entscheidend, die Regeln der Broker und alle geltenden Vorschriften einzuhalten, um Sanktionen oder Kontosperrungen zu vermeiden.

Häufig gestellte Fragen (FAQ)

F1: Welche Mindest-Infrastruktur wird für Latenz- oder News-Arbitrage beim US30 benötigt?

A: Mindestens benötigen Sie Zugang zu mehreren Brokern oder Datenfeeds, einen Low-Latency-VPS nahe dem Broker-Server und automatisierte Software zur Echtzeit-Analyse und Orderausführung. Für News-Arbitrage ist eine direkte Anbindung an Premium-Newsfeeds und FIX API sehr zu empfehlen.

F2: Wie häufig ändern sich die Offsets zwischen US30-Quotes?

A: Die Offsets können sich mehrmals täglich ändern, besonders während wichtiger Nachrichten, bei volatilen Marktbewegungen oder zum Handelsbeginn und -ende. Eine automatisierte Neukalibrierung ist für genaue Signalerkennung unerlässlich.

F3: Wie gleiche ich Lotgrößen zwischen verschiedenen Indizes oder zwischen CFDs und Futures korrekt ab?

A: Prüfen Sie immer die Kontraktgröße jedes Instruments. Hat z. B. ein US30-CFD eine Kontraktgröße von 1 $/Punkt und ein YM-Future-Kontrakt 5 $/Punkt, eröffnen Sie zur Risikoangleichung fünf CFD-Lots pro Future-Kontrakt. Prüfen Sie auch die minimal zulässige Lotgröße bei jedem Broker.

F4: Kann ich Indexarbitrage-Strategien bei Retail-Brokern nutzen, oder benötige ich institutionellen Zugang?

A: Viele Strategien sind bei Retail-Brokern mit schneller Ausführung möglich (z. B. cTrader, MT5, FIX API), aber für Futures-Trading oder Premium-Newsfeeds ist oft ein institutionelles Konto oder ein Drittanbieterdienst erforderlich.

F5: Was sind die wichtigsten Risiken bei der Indexarbitrage?

A: Zu den Hauptrisiken gehören Ausführungsverzögerungen (Slippage), Liquiditätslücken, plötzliche Spread-Änderungen, Brokerinterventionen oder -sanktionen, fehlerhafte Offset-Kalibrierung und Swap-Gebühren – insbesondere Dreifach-Swaps bei Übernacht-Positionen.

F6: Wie reagieren Broker typischerweise auf Arbitragehandel?

A: Einige Broker tolerieren Arbitrage, andere verhängen Beschränkungen, weiten Spreads aus oder sperren sogar Konten, bei denen sie systematische Arbitrage vermuten. Es ist wichtig, Handelsmuster zu verschleiern und die Broker-AGB strikt einzuhalten.

F7: Ist Indexarbitrage legal?

A: Indexarbitrage ist als Handelsmethode grundsätzlich legal, aber es ist unbedingt erforderlich, die Geschäftsbedingungen jedes Brokers sowie die geltenden Handelsvorschriften des eigenen Landes einzuhalten.